There are ways to get the most money for your timepiece, quickly and safely. My No. 1 recommendation is Worthy.com, an online auction platform rated B+ by the Better Business Bureau.

Worthy is an online marketplace, and each watch auction attracts bids from hundreds of qualified buyers all around the country — if not world. Worthy works with leading watch experts to accurately value each timepiece, takes professional, 3-D photographs using specialized digital equipment, and merchandises each watch. You control the reserve price, and are paid within a few days of the sale.

Most of Worthy’s buyers prefer brands whose watches retail for tens of thousands of dollars (and sometimes more).

Though Worthy.com is my top choice, there are other places to sell a watch to consider.

Sites including Worthy, WPDiamonds, and other online marketplaces and jewelry auctions can help you get a fair price for your watch. Benefits of selling online include ease of use, transparency and privacy — you don't have to be embarrassed walking into a local jeweler or pawn shop.

Online platforms also typically have lower overhead than brick-and-mortar jewelers or other businesses, so they have the margins to offer you higher prices — and are incentivized to do since the competition online is higher than in local markets.

2. Search for “sell watches near me” or “watch buyers near me”

You may find reputable jewelers, pawn shops, watch buyers and retailers in your area via Yelp, Google or other listings. One way is to use “near me” in your searches to find local watch buyers. You might also want to ask around for a recommendation.

3. Scrap metal buyers

If you have a gold watch that can be melted for scrap, send it to CashforGoldUSA.com, which has an A+ with the Better Business Bureau, pays within 24 hours and pays a 10% bonus.

CashforGoldUSA buys all kinds of watches, gold and silver jewelry, coins and silverware as well as diamond rings, necklaces, bracelets, earrings and other jewelry — and they pay within 24 hours of receiving your item.

4. Pawn shops

You may consider pawning your watch to a pawn shop near you, although it may be better to sell your jewelry online. Online gold buyers may pay more, as pawn shops typically pay 25% to 60% of the retail value of your item.

5. Consignment shops

Jewelry stores and antique shops both may purchase your estate and vintage jewelry and watches — either for a flat rate or on a consignment agreement.

Consignment shops typically accept an item for consignment and then pay the original seller a percentage of the sales price if and when the item sells. Online consignment sites like TheRealReal deal in fine jewelry and higher-end watches.

Expect consigning your watch to take longer than pawning and direct sales or online sales.

6. Facebook Marketplace

Facebook Marketplace has become a bonanza of buying and selling any number of goods and services, including timepieces. Simply post your watch with a few pics, a thorough description and suggested price — and then try to figure out which responders are scammers, crazy or potential buyers!

7. Give it away

You may want to give your watch to a family member or close friend, leave it to them in a will or your estate plan, or donate it to a charity thrift store.

Watch buyers near me and online

Top watch buyer: Worthy.com

Worthy is a leading marketplace that will do the heavy lifting of marketing your watch or fine jewelry to its network of professional buyers. Worthy.com will also have your watch authenticated by Watch Central, a partners specializing in timepieces.

Worthy.com chooses which brands to buy based on their buyers’ preferences.

Here’s a list of watch brands that are in demand by Worthy’s buyers:

In fact, unlike retailers who carry these brands, many of whom sell only newer watches, Worthy’s buyers actually prefer vintage or antique versions of these big names – particularly ones in excellent condition.

The rarity ups the value, which increases the amount you’ll be paid. So, that watch of your grandfather’s … ?

Once you decide you want to part with your watch, go to Worthy.com.

Go to Worthy.com

Get an online quote from a site like Worthy to understand if their estimate is in line with a price you feel comfortable with.

If they and you are interested in proceeding, Worthy sends you a free FedEx mailer overnight.

Send in your watch, 100% insured up to $100,000 by Lloyds of London.

Your timepiece is authenticated by Central Watch, a New York City watch repair, appraiser and buyer founded in 1952.

Worthy will professionally clean and digitally photograph your watch in special, high-definition images. You set the minimum price you are willing to sell.

Your auction goes live to hundreds of vetted buyers globally.

Get paid within as little as 24 hours by Paypal, or by check mailed to your home. Total sale time from sending in your timepiece to getting paid is about two weeks.

Worthy has a B+ rating with the Better Business Bureau.

When your watch or other jewelry sells, Worthy.com takes a fee of up to 22 percent of the sale price.

That’s something to keep in mind, but remember that anyone selling anything for you is going to take a cut.

Worthy scores points with its transparency.

If your jewelry doesn’t get sold for at least your reserve price, Worthy will return it for free, and you don’t wind up paying anything before the sale.

Second best watch buyer: myGemma

myGemma, formerly WP Diamonds, specializes in diamond jewelry, as well as luxury timepieces, handbags, and accessories. Their model is straightforward purchases, especially if you already have receipts or lab reports from your item.

Jewelers often appraise and buy fine and luxury watches of all kinds — it really depends on the jeweler and the market. A jeweler can be a good place to start to learn about your timepiece and get an initial offer. A jeweler is also helpful in providing an appraisal for insurance purposes.

Where is the best place to sell a watch?

Many people chose to sell their watch locally to a jeweler or watch collector who they know and trust, or who comes recommended.

There are many benefits to using one of the reputable online watch buyers. Online buyers tend to work in large volume with connections globally — which is really the scope of the international watch market.

Watch sellers find it useful to easily check sites like Better Business Bureau and Trustpilot for online businesses since the established ones can have hundreds or thousands of reviews and ratings.

Online businesses potentially can work on smaller margins, and pass those savings on to the seller, given they are not beholden to expensive retail real estate.

Further, many watch and jewelry sellers prefer the privacy and anonymity of selling their watch for cash, from home where there is no chance of running into a neighbor during the transaction!

Where can I sell my Apple watch?

Apple and other digital watches fall into another category entirely, though you can certainly resell your Apple watch for cash. eBay, Gazelle or even locally on Craigslist or Facebook Marketplaces are good places to sell watches. Pawn shops and consignment stores are also places to sell electronic watches.

Many local jewelers will buy your timepiece. First, do your best to understand your watch's value, and then make an appointment with a few local jewelers, to see who offers you the best choice. Many people prefer to sell jewelry and watches locally to businesses they know and trust, and negotiate face-to-face.

Where is the best place to sell a watch?

Selling your watch online is our No. 1 recommendation. Online buyers can reach an international market, have less overhead since they do not rely on expensive retail rent, and have the capacity to do large volumes of deals, allowing for smaller margins — which are passed along to sellers.

Where can I sell my Apple watch?

Apple and other digital watches fall into another category entirely, though you can certainly resell your Apple watch for cash. eBay, Gazelle or even locally on Craigslist or Facebook Marketplaces are good places to sell watches. Pawn shops and consignment stores are also places to sell electronic watches.

If you live with consumer debt, you are not alone. According to Federal Reserve data1, U.S. households have on average $6,300 in credit card debt and $33,090 in student loans, while the Consumer Financial Protection Bureau reports that a full 52% of credit bureau filings are for medical debt. Single mothers are especially likely to struggle with poverty.2

Mama, if you find yourself drowning in debt, rest assured you are not alone. But don’t use this fact as an excuse not to work like crazy to pay off your debt. If you live month-to-month owing others money, then the money you earn is not really yours. You are enslaved to your debt.

You are not the only person asking:

How do I get out of debt if I'm broke and have no money?

How do I get out of debt so I can stop living paycheck to paycheck?

How do I get out of debt with no money and bad credit?

This post gives a 9-step plan for reducing and paying off your debt.

As you figure out how to get out of debt on a low income, keep in mind that not every step on this list will reflect your situation. Follow as many as you can to get the best results:

1. List your debts, expenses, and income

Time to look the personal finance monster in the eye and lay out the FACTS.

Collect statements for each and every one of your debts: credit cards, medical bills, student loans, car note, mortgage, home equity line, personal loans from your parents or cousin.

Create a list of all your debt, including interest rates, monthly minimum payments and any deadlines.

My favorite app to help make this as simple as possible is You Need A Budget (YNAB). This app automatically pulls in all your income, debt, and expenses from your bank accounts. From there, you can set goals — and reach them! No matter what your financial goals are, it is so handy, so satisfying to see all these numbers in one place, and watch them move to meet your goals, day after day.

Chances are, mortgage rates have fallen since you first got your mortgage.

Transfer your credit card debt to 0% or lower APR:

See if you qualify for a 0% balance transfer credit card for a limited period, such as three or 12 months. Depending on your credit score, you may qualify for credit cards with lower rates long-term. This is a great way to pay off debt, as you save on interest along the way.

It only works if you are very organized, read all the fine print, and make sure you pay the premiums on time, and either pay off the balance or transfer the balance before the end of the promotion period.

But be honest with yourself: If you are not good with this kind of bookkeeping, this might not be a good option for you.

3. Negotiate interest rates with creditors

How to lower interest rates on credit cards

Another way to get a better rate on your card is to call your current credit card company and simply ask for a better rate. Here is a script:

“Hi, as you can see I am a longtime cardholder, and I love using your product. I am committed to paying off my debt and improving my credit history, and I'd love to stay with you. However, I need a better rate on my balance. Based on my research, I can get a [insert honest quote you received from another card] rate. Can you match it or do better?”

If your current card refuses to give you a better rate, research a 0% balance transfer credit card with another company.

Negotiate medical and other debt

Call the holder of any outstanding medical bills and negotiate.

4. Create a monthly budget of all your expenses and debt payments

Figure out how much you can afford to pay toward your debt by setting up a budget.

It is time to get serious, cut out any extra spending, and lower your overhead. Remember: Overspending is how you got in this pickle in the first place. Imagine how AMAZING it will feel to be debt-free! Check your student loan information at the National Student Loan Data System.

5. Choose a method for paying off debt: Debt snowball vs avalanche

When it comes to eliminating debt—whether credit cards, personal loans, student loans, or other debt—there are a number of popular strategies that you can employ. Two of the most common strategies, which you may have heard of, are the Debt Snowball and the Debt Avalanche.

While both are highly effective, each is better suited to helping you achieve different goals. Below, we take a look at each option to understand which will best help you reach your money goals.

Debt snowball is a debt repayment method to pay off credit cards or loans with the lowest balances first.

Finance guru Dave Ramsey made the debt snowball method popular, and for good reason: The advantage is that you get the psychological and emotional thrill of paying off accounts quickly. Imagine if you could actually remove a whole credit card account from your life?

Here is how to use the debt snowball method:

List your debts from smallest balance to largest balance — regardless of interest rate.

Make minimum payments (set up autopay) on all your debts except the debt with the smallest balance.

Pay as much as possible on your smallest debt.

Repeat until each debt is paid in full.

In the debt snowball method, you start by paying off the loan with the lowest balance first. This is beneficial for a number of reasons:

First, paying off any debt will give you a psychological “win” that you can use to propel yourself forward and continue hitting your goals. It stands as proof: You can do this! By paying off the debt with the lowest balance first, you’re getting this satisfaction quicker, which can help you stick with it for the long term.

Second, paying off the lowest balance will allow you to free up money in your budget. You can use this money to live a more comfortable life—or, ideally, to continue paying down your remaining debt.

How it works:

First, list out all of your debts, from smallest balance to largest balance. Ignore any other factors, such as interest rate.

Continue making your regularly scheduled minimum monthly payments on all of your debts. You don’t want to fall behind on anything—that can destroy your credit score!

Each month, pay as much extra as you can on the loan with the smallest balance. This will drive down the balance, saving you money in interest payments.

Once the debt with the lowest balance is paid off, take note of the minimum monthly payment you were paying toward it. Roll that amount over into the loan with the next lowest balance, so that you’re paying more toward it. Continue paying as much extra each month as possible.

Repeat until you have paid off all of your debts.

The method gets its name from the way that a snowball continuously grows as it rolls down a hill. As you pay off each debt, you free up more money each month that you can apply to the next debt. By the time you’ve got a single loan left, you’ve got the collective power of all of the money you’ve freed up, like a runaway snow-boulder!

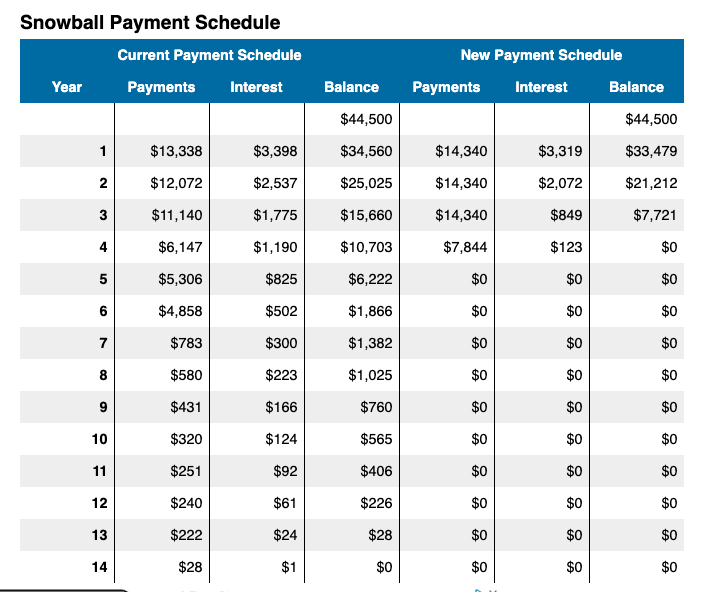

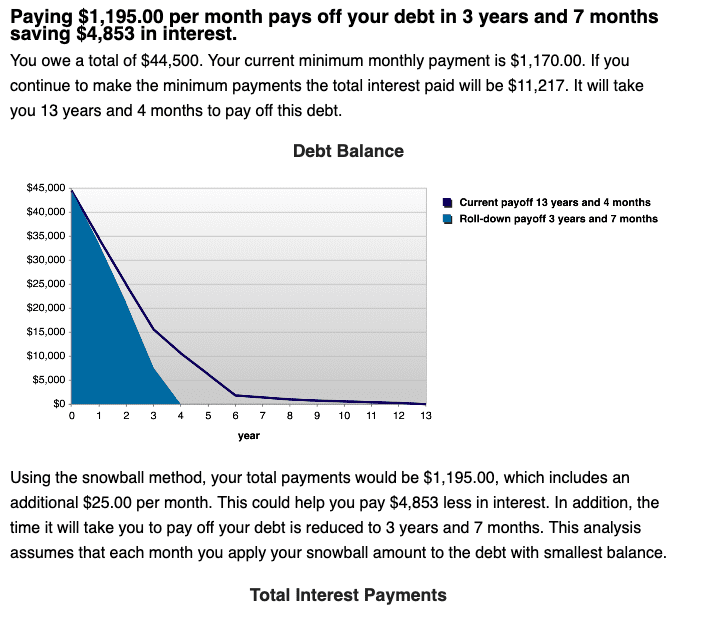

In the example below, this mom has $44,500 in combined credit card, car, and student (“Other”) debt.

Using the snowball debt payment method, you can see here how quickly she was able to pay off her debt, compared with if she were to simply pay the minimums on each of these four accounts:

In the example below, this mom has $44,500 in combined credit card, car and student (“Other”) debt:

Using the snowball debt payment method, you can see here how quickly she was able to pay off her debt, compared with if she were to simply pay the minimums on each of these four accounts:

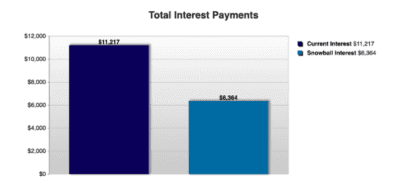

Using the snowball debt program, she slashed her debt to $0 in 3 years and 7 months, compared with 13 years!

This quicker, more aggressive repayment saved her $4,853 in interest.

What is the debt avalanche method?

In the debt avalanche method, you instead start by paying off the loan with the highest interest rate first, regardless of how large the balance is.

The key benefit behind the debt avalanche is that by paying down the balance with the highest interest rate first, you are saving the most money over the life of the loan. While you won’t necessarily have the psychological perk that comes with paying off a low balance, it can still be incredibly empowering to know that you’re sticking it to the banks and reducing their ability to profit off of you.

How it works:

First, list out all of your debts, from the loan with the highest interest rate to the loan with the lowest interest rate. A budgeting tool like You Need A Budget can be incredibly helpful.

As with the debt snowball, continue making your regularly scheduled minimum monthly payments on all of your debts.

Each month, pay as much extra on the loan with the highest interest rate. As the balance decreases, you’ll pay less in total interest over the life of the loan.

Once the debt with the highest interest rate is paid off, note the minimum monthly payment that you were paying on it, and apply that towards the loan with the next highest interest rate. Continue paying as much extra each month as possible.

Repeat until you have paid off all of your debts.

As you pay off more and more of your debts using this method, the amount that you save each month will compound into an avalanche of savings.

A single mom I know budgets $500 toward debt payoff. She uses YNAB to document her debt goals and strategy, and to create a budget. Her loans include:

$1,000 due on a credit card debt with a 20% interest rate

$5,000 left on her student loans, with an 8% interest rate

$1,250 monthly car payment at a 6% interest rate

To keep things simple, let's say each debt has a minimum monthly payment of $100.

This mom will set her car and student loan payments to the minimum of $100 each.

The remaining $300 of her monthly debt budget is devoted to her highest-interest debt: the credit card at 20%. The card debt will be entirely paid off by the third month. Whoo hoo!

Now, the extra $300 (plus the current $100 minimum = $400 monthly) goes toward slashing the second-highest interest-bearing debt: the student loans. That will be paid off after 1 year and 1 month. Yay!

Finally, all $500 goes to the debt with the lowest rate of interest, the car loan, which will be paid off three months later.

Congratulations, mama!

Debt snowball vs. debt avalanche

In choosing which method you pursue, it’s important to know the personal goals behind your debt elimination journey. Specifically, what are you trying to accomplish?

The debt snowball method might be right for you if:

You want a quick psychological win

You need to prove to yourself that you can pay off your debt

You need to free up money in your budget for other expenses

The debt avalanche method might be right for you if:

You don’t mind potentially going years before you pay off your first balance

You want to save as much money as possible

You have a moral disposition against interest

It’s also important to note that you don’t necessarily need to commit fully to just one method. If you decide to pursue the debt avalanche method, for example, that’s great.

But if you’re working on it for two years and begin to feel burnt out or weary, go ahead and pay off the loan with the lowest balance! It’ll give you the boost that you need to return to the avalanche method and commit for the long term.

Additionally, there may be other factors that you might want to take into consideration. For example, if you’re paying off your student loans, do you have a mix of unsubsidized and subsidized federal loans?

If so, paying off your unsubsidized loans, which come with fewer benefits, may be the wiser move—regardless of interest rate or balance.

Ultimately, snowball vs. avalanche debt payoff is about which one feels best for you, and which plan you are more likely to stick to!

6. Sell stuff to earn money to pay off debt

As long as you are cleaning out debt, you might as well also cleanse your closets, drawers, garage and basement. Declutter your home, sell unwanted stuff, and put that extra cash towards your debt paydown program. Here are some things you can sell:

Hiring a professional resume writer or resume editor is a huge advantage. A quality resume service will help you not only create a professional resume, but also help you frame your experience and goals in a way that you cannot do on your own. It always helps to have a second set of trusted eyes when it comes to important career moves. Get a free resume review >>

If you’re totally overwhelmed with the debt-payoff process—or truly believe that you cannot dig out of debt on your current income—professional services can help.

A professional debt-relief service can help if you have:

Large sums of medical debt that you have no immediate way of paying off

So many loans and credit cards that you can’t manage on your own, and you may even be considering a hardship loan just to stay afloat

Poor credit, which means high interest rates, which makes payoff even harder, and you don't know where to start to stem the chicken-and-egg problem

Debt relief services will negotiate down some of what you owe in exchange for a fee of 25% or more. The sum that is reduced is likely taxable, but it may still be a good deal. Here are some of the more reputable tax relief companies:

By comparison, a debt consolidation company will consolidate all of your debt into a single payment with a lower interest rate than all of your debt combined. The benefit is a shorter repayment term, fewer individual bills to manage, and less interest paid over the long-term.

Meanwhile, if you have poor credit, a credit repair company can help by disputing old or erroneous negative credit items, and counsel you to repair your credit history and score — which will help you qualify for a mortgage, car loan or better terms on existing credit:

Alternatively, if you only want to speed up the process of paying off your credit card debt, you can opt for credit card consolidation, unify the debt from different card issuers, and pay them off slowly.

Correct errors on your credit report

Legally, every person in the United States is entitled to correct errors on their credit report. It is not uncommon for your score to be hurt by old debts that have actually been paid off (but still appear on your report), debts or bankruptcies that are not yours, or legitimate debts that erroneously are reported multiple times.

Getting these red marks off your credit report is within your legal rights, but it can be a huge pain in the butt. If you are strapped for time and patience, it can be worth the investment to pay a reputable credit repair company to take over this task for you.

9. Be honest with yourself about your personal finances

If you are stressing about your debt and credit, likely you are avoiding the facts of your financial situation. Below I will show you how to easily manage all your debt, bills and income, but first you have to deal with the emotional side of this problem.

Facts are that financial stress is REAL, and it takes a toll on your relationships, physical health and mental health. You may join those of us who struggle with deep money issues stemming from childhood, and therapy may be in order.

Be honest with yourself about how your money situation makes you feel. Living paycheck-to-paycheck is really stressful, right? Moving money around each week to make sure some bill clears is a shameful waste of energy and time. Living beyond your means is scary. Not having control of your money is embarrassing. Own all those feelings. They are normal, and they are real.

Face the facts about how you got here. It is easy to blame your parents for not teaching you about money, or the federal education system for failing to make personal finance mandated schooling, or banks for ripping people off, or your boss for underpaying you, or your ex for screwing you in the divorce, or your friends for pressuring you to overspend.

Ultimately, you are responsible for your money. You are smart and resourceful, and trust me: dumber people have gotten out of debt and even gotten really stinking rich. You can figure this out, and I will help you. But first, you have to own your responsibility in this mess.

Focus on the future. Think about how incredible it will feel to have all your bills set up on autopay, and never think about them because there is plenty of cash in the bank. Imagine how amazing you will sleep knowing you and your kids' future is secure. Visualize how powerful you are each day as you make decisions about your career, your children, your home and your life.

FAQs about how to pay off debt on a low income

How do I get out of debt if I have no money?

Here are your options to get out of debt:

Budget, cut back your expenses and pay off your debt over a long, systematic term on your current budget

Find ways to refinance and consolidate your current debt

Earn more money while maintaining your lifestyle, putting any extra money towards your debt first, even before savings and investments.

If you have reason to believe that you truly cannot ever get out of your personal debt, consider bankruptcy.

How do I get out of debt if I live paycheck-to-paycheck?

If you feel you don’t have any extra money to pay off your debt, your options include:

Refinance your credit card, student, auto and mortgage debt.

Lower your monthly bills. This might include moving into a lower-cost home, getting a roommate, refinancing your mortgage or car, canceling some subscription services, adopting a more affordable lifestyle (less eating out, less shopping or vacations), as well as refinancing your credit card debt, tax or student debt.

Earn more. Can you negotiate a raise, get a new job, start a side business or side hustle?

In extreme situations, you may qualify to discharge some of your debt through bankruptcy.

More debt relief resources for single moms (and anyone struggling to make ends meet)

A credit counselor can advise you on your financial situation and debts and help you put together a feasible budget. The Federal Trade Commission3 suggests finding a reputable nonprofit organization that offers free credit counseling services to help you get on track.

Here are a few to research:

American Consumer Credit Counseling — Offers a free debt counseling session

National Foundation for Credit Counseling — Provides online resources to help you learn about the debt management process and connects you to certified financial counselors

GreenPath Financial Wellness — Offers free debt and credit counseling by phone

Debt Reduction Services — Shares do-it-yourself debt management tools but also offers a free session with a certified credit counselor

You can also contact your credit union, church, or a local charity to ask about debt counseling services.

Bottom line: Use these tools for how to get out of debt on a low income

The upside to the personal debt crisis is that there are tried and true methods for getting rid of it – and plenty of analog and tech resources to help. Even if you have a low income or are living on one income.

Here are some more resources if you have a low income:

“Changes in U.S. Family Finances from 2016 to 2019: Evidence from the Survey of Consumer Finances,” Federal Reserve Bulletin, September 2020, Vol. 106, No. 5. Board of Governors of the Federal Reserve System. federalreserve.gov/publications/files/scf20.pdf

“The Changing Profile of Unmarried Parents,” by Gretchen Lingston. Pew Research Central, April 25, 2018. pewresearch.org/social-trends/2018/04/25/the-changing-profile-of-unmarried-parents/

“How To Get Out of Debt,” Federal Trade Commission Consumer Advice. https://consumer.ftc.gov/articles/how-get-out-debt

How do I get out of debt if I have no money?

Here are your options to get out of debt: cut back and pay off your debt with your current budget; reduce or consolidate your current debt; and earn more money while maintaining your lifestyle.

Who can help me get out of debt?

A debt or credit counselor can help you create a plan to get out of debt.

Single women accounted for 20% of first-time, and 18% of repeat home buyers in 2021, according to the National Association of Realtors. That same year, a Freddie Mac study found that 58% of single female head of household renters didn’t believe they would be able to afford a home.

Even though the journey to homeownership has its challenges, it is possible for single moms to buy a home with the right knowledge and resources, including steady employment. And home ownership has many benefits, like equity and tax deductions. However, while preparing for homeownership, some individuals may explore short-term financial solutions to manage temporary expenses or cash gaps before securing long-term mortgage financing.

Keep reading to discover affordable mortgage loan options and education programs to help single moms with aspirations of homeownership:

Let’s face it. If you’re a single mom, it can be hard to buy a home. The most obvious hurdle is your financial situation, since you’ll be buying a house on one income.

And even though the gender pay gap is narrowing, women are still earning less than men according to the U.S. Census Bureau. Women consistently make 30% less in annual income than men, and that number creeps upward as women age.

“Buying a home is never an easy process, and being a single mom makes it more difficult — but not impossible,” says Zackary Smigel, real estate expert and creator of the real estate education program, Real Estate License Wizard.

Smigel, a licensed realtor and mortgage broker, points out that single moms with low incomes can take advantage of home-buying assistance programs.

These programs often have low loan interest rates or offer grants that don’t require repayment.

Apply for low-income home loans such as Freddie Mac Home Possible and Fannie Mae HomeReady. You can find these programs by attending home buying seminars, talking to lenders and real estate agents, or searching for “low income mortgages” online.

Connect with organizations and nonprofits like Habitat for Humanity which builds affordable homes for qualified applicants who are willing to help build the house and can pay a mortgage that does not exceed 30% of the person’s income.

If you have another single friend or family member who is looking to buy a home, you can also discuss pooling your resources to buy one together.

You can also create a housing fund and ask friends and family to contribute to it in lieu of gifts for birthdays and holidays. Sites like GoFundMe make it easy for people to help.

Low-income home loans

There are a lot of home loan options available for low-income households. Learn more about these helpful programs so you can choose the best fit. Ask your preferred lender which programs they offer for creditworthy, low-income borrowers.

As a borrower, your income must be 80% of the area median income (AMI). You can use the Fannie Mae AMI lookup tool to check your geographic area’s AMI.

You’ll need a minimum 620 credit score to apply, though 680 can unlock better rates. Down payment options are as low as 3% and funding from relatives, grants, and Fannie Mae Community Seconds is allowed. There are no geographic restrictions.

You can get reduced mortgage insurance that cancels when the loan balance falls below 80% of the loan-to-value (LTV) ratio (the amount of the mortgage versus the value of the property). Finally, you must take the Fannie Mae HomeView online course or an approved alternative HUD-approved course to be eligible.

Operation HOPE Home Buyers Program helps low-income home buyers through FDIC-approved loans, down payment assistance, and first-time buying assistance.

Operation HOPE offers multiple programs to increase financial knowledge in underserved communities. Its first-time home buyer education program provides HUD-certified coaches to guide you through the home loan process.

You’ll get group training as well as one-on-one coaching that extends beyond the classroom. When you are ready to pursue an FDIC loan, your Operation HOPE team will continue to provide support. They can also connect you with other professionals along the way.

Check into getting a Federal Housing Administration (FHA) loan, which offers lowered closing costs and down payments. The FHA offers fixed-rate loans available in 15- and 30-year terms nationwide.

Borrowers enjoy low down payments and closing costs. It’s ideal if you have moderate to low income and a low credit score.

With a score of 500 to 579, you'll need a down payment that is 10% of the cost of the home. At 580 or more, you’ll only put 3.5% down.

With an FHA loan, you must pay mortgage insurance, and if you put down less than 10%, you will pay it for the life of the loan.

The property you want to buy must meet FHA eligibility requirements. For example, the FHA loan limit range for homes across the country is $472,030 to $1,089,300. You can check your specific area with this FHA lookup tool.

If you’re looking for low income home loans for single mothers, a Freddie Mac Home Possible mortgage could be right for you. With as little as 3% down, you can become a homeowner. To be eligible, your income cannot exceed 80% of the area median income (AMI).

There are no geographic limits on loan amounts, and you can apply even if you do not have a bad credit score due to lack of credit history (though approval isn’t guaranteed). Mortgage insurance is required on one-unit properties, but once your loan balance is less than 80% of its value, it is no longer required.

5. Fannie Mae

HomePath properties are Fannie Mae-owned homes offered to the public at a discount after the previous owner defaulted on a Fannie Mae-owned mortgage. These mortgages come with low down payments, renovation loan eligibility and closing cost assistance of up to 3% of the home’s purchase price.

If you are an active duty or reserve member of the armed forces, veteran, or eligible spouse, a VA loan could be the best way to go. If approved, you won’t need to provide a down payment or mortgage insurance. Plus, closing costs are kept to a minimum. There are no loan limits if you can afford the property.

The VA guarantees part of the loan and works with private lenders to offer affordable interest rates. The VA loan is available in every state and tribal lands via the Native American Direct Loan (NADL).

The U.S. Department of Agriculture helps rural borrowers refinance their mortgages. This offer, in response to borrowers who did not have to pay a monthly mortgage because of COVID-19, helps keep payments affordable once they resume.

These direct home loans are available for very low- to low-income borrowers who were approved for a mortgage payment stoppage due to COVID-19. You must meet or fall below the income limits for your area to be eligible. Your credit score is not a factor unless you have substantial federal debt.

The USDA Single Family Housing Guaranteed Loan Program offers a year-round application process. If you live in a rural area, this loan provides a way to purchase or build a home with no money down for qualifying applicants. The program offers 100% financing from approved lenders because it guarantees 90% of the loan.

To be eligible, you cannot exceed 115% of the area median income (AMI). You can use this USDA tool to check eligibility for properties and income. There is no set credit score, but you must show a history of making an effort to repay any debts you have.

Habitat for Humanity fixes up and builds affordable homes. The nonprofit serves 50 states and about 70 countries. If you are willing to take home ownership classes, volunteer at a Habitat ReStore, or help build your own home (or someone else’s), you could be one of the next Habitat homeowners.

To be eligible, you must demonstrate a need to secure safe housing and be able to make affordable monthly payments.

Are there any home buying programs for single moms?

In addition to low-income mortgage loans, there are also home buyer programs for single moms, which can help to find affordable properties and programs that offer mortgage assistance. Some lenders also offer low credit home loan options designed for buyers who are rebuilding their credit, making homeownership more accessible even if your score isn’t perfect yet.

Some of these federal, state, and nonprofit home-buying programs also educate you on the home-buying process from beginning to end.

Check out the following resources for single moms:

Department of Housing & Urban Development (HUD)

You buy a home directly through HUD. In fact, a key purpose of HUD is to help more people become homeowners.

HUD properties are lower priced because they are foreclosures or defaulted properties. They are owned by HUD as a result of a foreclosure on an FHA mortgage and are currently available in most states, although inventory changes constantly.

To buy a HUD home:

Contact your local HUD counseling agency

Work with a lender to find out how much you can afford

Choose the right mortgage type based on your circumstances

Use the HUD inventory list to search for your new home

Make an offer and prepare for the closing upon acceptance

HUD offers an online homebuyer’s kit that details the homebuying process. If you need help or have questions, you can contact a HUD housing counselor. They offer free or affordable advice to guide you through the process.

Public housing authority

Your state housing authority may have leads on local homeownership programs. Some may be designed especially for single parents. These programs, run by HUD, usually require counseling for prospective homeowners.

For example, under the Section 32 homeownership program, a PHA may sell one or more units in a public housing development to a low-income family. Plus, the PHA can offer Capital Fund assistance to help the family buy the home.

The Capital Fund is administered by the Public Housing Investments (PIH) Office of Capital Improvements. Each year, it awards grants to PHAs so that they can assist prospective homeowners as well as improve and update public housing developments and management systems.

The Chenoa Fund is a government-chartered organization that provides up to 5% down payment assistance for those with a FICO Score of 600 or higher. The financial help can go towards a down payment, closing costs, prepaid items or you may direct funds to all three.

You are eligible for the best pricing if your income is less than 135% of your area’s median income.

The Chenoa Fund offers two options: a 10-year fixed-rate repayable loan or a 30-year forgivable loan. The 30-year loan has a 0% interest rate, requires no monthly payments and is forgivable under these conditions:

A 3.5% loan is forgivable when you pay your mortgage on time for 36 consecutive months

A 5% loan is forgivable after you make 120 payments on your primary mortgage.

Community Seconds

Community Seconds is a Fannie Mae-approved second mortgage that allows you to use the funds available from state and local governments as well as housing nonprofits to put together a down payment, get help with closing costs and even complete minor renovations.

Single mom home loans FAQs

Does my state have a homeownership assistance program?

Every state has some type of program to help homeowners — from government programs to private and nonprofit options. To find local help, start with a Google search on “homeowner assistance programs near me” or “first-time home buyer help in (your state).”

Find state-based programs offering assistance with down payments, closing costs, and special financing options.

How can a single mom build a house?

Check with organizations like Habitat for Humanity. They build houses with affordable mortgage terms. You can apply and have a chance to help build your own home.

The FHA and USDA also provide home loans you can use for new construction.

How can a single mom get home loans with bad credit?

If your credit score is bad, you’ll want a home loan that does not require a credit score or has options for low credit scores (less than 600).

For example, VA loans don’t require a minimum credit score or down payment, and FHA loans have options for single moms with a score of at least 500.

Home Possible® home loans from Freddie Mac also don’t require a credit score to apply.

How do I clean up my credit to buy a house?

A good credit score is important for buying a house. Fortunately, there are ways to fix bad credit. Here’s how to build your credit systematically:

Keep an eye on your credit score and report. Once your score reaches 700 or more, move on to a regular, unsecured credit card — one with no annual fee, a good points system, and other perks that you can now enjoy thanks to a solid credit score!

Get a co-signer with good credit for a regular credit card. Their good credit will affect your credit.

Become an authorized user on the credit card of someone with good credit, such as a parent, friend, or mentor.

Be a good credit user. Keep the total borrowed at 30% or less of the credit limit.

Make all of your monthly payments on time. The most important factor that makes up your FICO score is your payment history. As a result, you need to make it a priority to make all your monthly bills on time. Learn how to get help with energy assistance costs.

Dispute inconsistencies and errors on your credit report. If you find errors or downright lies, make sure to dispute them via the formal process offered by the Federal Trade Commission (FTC). You may choose to hire a credit repair company to do this for you.

As your credit score improves, you’ll be able to apply for some of the home loans mentioned earlier in this post.

What is the fastest way to raise your credit score to buy a house?

If you do not have any recent credit history, you can build a good credit history with the credit rating company FICO, within six months.

Tools to quickly raise your credit score now:

Secured credit cards. A secured credit card requires you to put down a cash deposit to secure your own credit line — and as long as you make regular charges, and regular payments on time, your score will increase quickly.

Check your credit report and FICO score for free, and see if you qualify for an immediate credit score increase of up to 20 points with Experian Boost, a legit way to boost your score.

Can I get help with my mortgage if I am a single parent?

Home loans will help you to fund the purchase of your home, but you may be wondering how you can afford a mortgage payment, and if help is available.

Fortunately, there are mortgage assistance programs for single mothers:

If you have a Fannie Mae home loan, you can get mortgage payment help such as forbearance or loan modification. Use the Fannie Mae lookup tool to search for options.

If you have a Freddie Mac home loan, you can use this lookup tool to learn about helpful programs to keep you in your home.

The Homeowner Assistance Fund (HAF) is a federal program that helps homeowners pay their mortgages if they can prove financial loss from COVID-19. The HAF program is closed in Alaska and Florida.

If you have an FHA loan, HUD offers a list of resources to help you stay in your home if you have trouble making the mortgage payments, such as the Making Home Affordable (MHA) program.

You can also contact your mortgage lender and inquire about foreclosure prevention programs.

What are hard money loans?

Hard money loans are short-term real estate loans secured by the value of the property itself, rather than the borrower's creditworthiness. These loans are typically provided by private lenders or specialized companies and are known for their speed and flexibility, though they come with higher interest rates and shorter repayment terms than traditional loans.

Bottom line: Home loans for single mothers are available, along with assistance

There are home loans available for single moms. While loan amounts, interest rates, and fees vary, there is likely an option that will work for your financial situation. Plus, you can get assistance to pay your mortgage through grants, tax credits, and government programs.

Before, during, and after the home buying process, be diligent with your finances, which will help you to build credit or improve your credit score.

Research all options to find mortgage assistance programs that best suit your needs. You can also talk to an HUD housing counselor or enroll in a first-time home buyer class to get more information on assistance programs so you know what to expect as you start the process.

No matter your income, there are many programs to help single moms achieve homeownership. It can be an uphill battle to ensure you are financially capable of owning a home and making regular payments, but there are many programs available to help you buy a house as a single mom.

Does my state have a homeownership assistance program?

Every state has some type of program to help homeowners — from government programs to private and nonprofit options. To find local help, start with a Google search on “homeowner assistance programs near me” or “first-time home buyer help in (your state).”

How can a single mom build a house?

Check with organizations like Habitat for Humanity. They build houses with affordable mortgage terms. You can apply and have a chance to help build your own home. The FHA and USDA also provide home loans you can use for new construction.

How can a single mom get home loans with bad credit?

If your credit score is low, you’ll want a home loan that does not require a credit score or has options for low credit scores (less than 600). For example, VA loans don’t require a minimum credit score or down payment, and FHA loans have options for single moms with a score of at least 500. Home Possible® home loans from Freddie Mac also don’t require a credit score to apply.

If you can’t afford a cell phone or wireless service, there are programs that can help you get a free smartphone or cellphone. Here’s the best way to get a free phone or a discounted one:

Best way to get a free phone: Lifeline Assistance Program

The Lifeline Assistance Program is the main program that provides free smart phones and free or reduced-price wireless cell phone plans and landline service to low-income people. Lifeline is a federal program available in every state, territory, and on Tribal lands.

When you sign up for Lifeline, you can choose a free smartphone from many of the participating providers in this post. But Lifeline also helps you pay for your cell phone bill.

Lifeline gives you up to $9.25 per month to pay your cell phone bill. If you live on Tribal land, you can get up to $34.25 per month. This benefit applies to already discounted, low-income plans. In some cases, there is zero cost to Lifeline subscribers, as outlined through the different programs listed below.

You are eligible for the Lifeline Assistance Program if:

You receive assistance such as an EBT card, SNAP, Medicaid, or SSI.

How to get free phone service from Lifeline:

Apply online through a Lifeline administrator (list below).

Once you are approved for Lifeline, you are good to go for one year. Just use it at least once a month to keep it active. After a year, you must reapply to keep the service.

You can use your Lifeline benefit for one service per address and you can’t transfer your benefit to someone else.

Here are some of the wireless providers that work with the federal Lifeline Assistance Program to provide free or discounted government smartphones and wireless service:

Lifeline's Access Wireless is a legit service that offers free nationwide cell phone service for qualified Lifeline recipients. Buy a discounted iOS smartphone for as low as $149 or an Android cell phone for as low as $39. Bring your own compatible device and pay just $9.99 for a SIM card.

Access Wireless has an A+ rating with the Better Business Bureau (BBB).

AirTalk Wireless makes it possible for qualified Lifeline/ACP recipients to get a free touchscreen iOS or Android smartphone or wireless phone. AirTalk offers service and plans in 37 states and Puerto Rico.

AirTalk offers three plans:

Lifeline: 4.5GB of data, 1,000 talk minutes and unlimited texting, and free SIM that you can put in an existing smartphone (no free phone)

Lifeline/ACP: 15GB of data, unlimited talk and text, and free upgraded smartphone

ACP: 8GB of data, unlimited talk and text, and a free basic smartphone

AmericanAssistance provides qualified applicants with a free government touch-screen smartphone with a new monthly plan. The Lifeline/ACP program covers subscribers in 20 states and Puerto Rico. The ACP-only program covers seven states and Puerto Rico.

American Assistance also works with California Premium Lifeline, a state-based cell phone assistance program that offers free unlimited voice, text and 6GB of data monthly. There are no activation fees, contracts, or device deposits.

Assurance Wireless (now part of T-Mobile) offers new Lifeline and/or ACP Assurance Wireless customers a free Android smartphone.

The Assurance Wireless Lifeline/ACP plan gives you free data, and unlimited text messages and minutes. The Lifeline-only plan hooks you up with unlimited data, texts, 1,000 minutes, and 4.5GB of data with no activation fee or device deposit.

Assurance Wireless serves low-income residents in 42 states and has an A+ rating with the BBB.

AT&T works with ACP to deliver free and affordable high-speed data and unlimited talk and text on prepaid phone plans, including:

Free 5GB of data and unlimited talk and text

$10 per month for 15Gb of data and unlimited talk and text

$20 for unlimited data, talk and text (when you sign up for autopay)

AT&T doesn’t offer a free phone, but you can get a free SIM shipped at no charge when you bring your own compatible device. Or shop for a new prepaid phone through Walmart, AT&T’s mobile device partner. Activation fees vary by phone choice.

In addition, Access from AT&T is the carrier's low-cost internet service that costs $30 per month or less. Available in 21 states, AT&T's low-income program is available to those who meet ACP income requirements or who receive benefits from SNAP, SSI (only for California residents), or the National School Lunch Program (NSLP).

Cintex Wireless will give you a free Android or Apple smartphone of your choice with a $0/month plan with 15GB of data and unlimited talk, text, and picture messaging if you qualify for Lifeline and ACP.

Cintex Wireless offers this plan nationwide. There are no deposit or activation fees.

Plus, Lifeline/ACP-eligible customers get unlimited calling to Canada, Mexico, Argentina, Brazil, Colombia, Costa Rica, Guadeloupe, Paraguay, Peru, and Venezuela.

Separate Lifeline-only and ACP-only plans are still free, but have different features:

Lifeline customers can bring their own device and get a free SIM card. The free plan provides 4.5GB of data each month, plus 1,000 talk minutes and unlimited texting.

If you are only eligible for ACP, you’ll get 8GB of data plus unlimited talk and text.

Cintex Wireless has a profile but is not rated by the BBB.

Apply now at Cintex Wireless with your zip code to view plan options.

7. Easy Wireless

Easy Wireless provides eligible Lifeline and ACP customers free or discounted smartphones and free talk, text, and data.

If you qualify for:

Lifeline and ACP, you can get the Unlimited Plan. It comes with a free smartphone and unlimited talk, text, and data.

Lifeline-only, the Base Plan includes $25 smartphones and free text, 1,000 talk minutes, and 25 MB of data.

ACP only, you can get the Plus Plan that features a free smartphone, unlimited text and talk and 5 GB of data.

All Tribal Lifeline and ACP plans offer a free smartphone. Most include unlimited talk, text, and data.

Even if you don’t qualify for Lifeline or ACP, Easy Wireless has plans that start at $5.25 a month with 1,000 talk minutes, unlimited texting, and 25 MB of data.

If you already have a phone, you can bring it over to Easy Wireless. It only takes a few minutes to find out if your phone is compatible. There is no deposit or activation fee.

Easy Wireless has an A+ rating with the BBB.

Apply at Easy Wireless with your email and zip code to see all plan options.

8. enTouch Wireless

If you qualify for Lifeline and/or ACP, enTouch Wireless offers a free Android smartphone with options for free unlimited data, talk, and text, or limited data plans with 5.6-11GB of data. There are no activation or device fees.

enTouch Wireless is available in 34 states and on Tribal lands. You can view eligibility requirements on the state list.

In some states, if you only qualify for Lifeline, enTouch offers a free SIM card for unlocked phones. The features of these $0/month plans and data limits vary by state.

This provider also offers free international calling from the United States to Canada, Mexico, the United Kingdom, India, China, Vietnam, and South Korea.

Infiniti Mobile provides free, nationwide mobile and broadband internet service for customers eligible for Lifeline and ACP. If qualified, you can get unlimited talk, text, and data on your own device or get a free phone with service.

Infiniti Mobile pricing on phone plans varies by state. With Lifeline and ACP, plans are free or at a reduced cost after applying the benefits. There are no activation fees and you can bring your own compatible device and keep your number.

If you qualify for Lifeline and ACP, you may be eligible for a free touchscreen government phone and a free or discounted monthly plan. Life Wireless’s Lifeline plans are offered in 36 states and Puerto Rico and U.S. Virgin Islands. ACP plans are available in 13 states and the District of Columbia.

Lifeline/ACP plans offer a free smartphone, a hotspot and free unlimited data, talk and text. Lifeline-only plans vary, but most give you 500 minutes per month or unlimited talk and text.

If you have ACP, you can get free unlimited talk, text, data, and up to 6GB of hotspot data use. No activation or device fees.

Q Link offers Lifeline/ACP nationwide, unlimited, free monthly cell phone service including data, minutes and text and picture messaging. If you qualify for ACP you can also get a new tablet. There is a one-time device fee of $10.01 for the tablet.

Q Link does not provide cell phones or smartphones, so you’ll need to bring your own phone to the wireless provider and you can keep your existing number. There are no activation fees.

Q Link has a profile with the BBB but it is being updated as of January 2024.

SafeLink Wireless works with Lifeline and ACP and is one of the largest low-income cell phone service providers in the nation, operating in most states and territories with no activation or device fees.

As a new eligible customer, you can get a Safelink free smartphone and unlimited phone calls, texting, high-speed data, and 10GB of hotspot data. If you already have a phone you like, you can transfer your number to SafeLink Wireless and still get free service.

SafeLink Wireless has been accredited with the BBB since 2014 and carries an A+ rating.

SafetyNet Wireless offers prepaid, free, and discounted smartphone plans. This company provides cell phones to low-income people through its participation with Lifeline, ACP, and California Lifeline.

SafetyNet Wireless is available in California, Colorado, Georgia, Kentucky, Louisiana, Michigan, Missouri, New York, Oklahoma, Pennsylvania, and Wisconsin.

California Lifeline plans costs range from $0 to $25 per month and offer unlimited talk and text and up to 12 GB of data. In other states, the monthly prices and data limits vary.

ACP plans offer free and discounted broadband internet service. This service also comes with a tablet that has a one-time device fee of between $10 and $50 depending on the device you choose.

StandUp Wireless works with Lifeline and ACP to offer a free or discounted government smartphone by mail you can self-activate with unlimited talk and text, unlimited extra data, and 10 GB of high-speed data each month.

Lifeline/ACP plans range from $30 to $110 per month (before your Lifeline/ACP discount) and offer unlimited talk, text, and data with up to 60GB of high-speed data.

If you are eligible for ACP, you can get a new tablet for as low as $10.01. StandUp Wireless does not offer phones for purchase, but you can bring your own compatible device and keep your number. StandUp Wireless offers 5G/4G LTE nationwide coverage. Use your zip code to see if it is available in your area.

StandUp Wireless was BBB-accredited in 2016 and has an A+ rating.

TAG Mobile participates with Lifeline and ACP and leverages Verizon wireless and T-Mobile networks. It’s available in 19 states and 11 cities in California.

In California, you can get a free smartphone with unlimited talk and text and up to 8GB of data each month. In other states, TAG Mobile provides a free monthly plan with unlimited voice, text, and 8.5GB of data. If you qualify for ACP you can purchase a tablet for as little as $10. There are no activation fees.

The program allows you to bring your own compatible phone, transfer your number, choose prepaid or monthly plans, and shop for phones all online.

Low-income people who qualify for the Lifeline program can get a free or discounted cell phone, free minutes, texting, data, 4.5GB of data, and nationwide calling every month with Tempo Wireless.

Tempo Wireless covers 22 states. Prepaid plans are available and there are no activation or device fees.

TerraCom Wireless offers a free smartphone and free monthly cell phone service to those who qualify for Lifeline in 21 states. Each state has different caps on monthly minutes, text messages, and data.

You can bring over your phone if you prefer to keep it. There is no activation or device fee. Broadband plans are also available.

T-Mobile provides free and discounted cell phone options and participates in Lifeline and ACP. For Lifeline-eligible customers, T-Mobile offers cell phone plan discounts to subscribers in Florida, Kentucky, Minnesota, Mississippi, Pennsylvania, Virginia, Washington, and Puerto Rico. Fill out and submit the T-Mobile form for Lifeline discounts.

For ACP recipients, you can get a free cell phone with a plan that ranges from $0-$30 per month (with ACP discount) through Metro by T-Mobile. All plans contain unlimited talk and text but data ranges between 5GB and unlimited depending on the plan you choose.

TruConnect offers cell phone plans, prepaid plans, broadband service, and hotspots, as well a range of Android and Apple phones and tablets at steep discounts or for free, and administers Lifeline and ACP wireless and cell phone programs.

With TruConnect, those qualifying receive a free Android phone, unlimited talk, text, and data, and free international calling to Mexico, Canada, China, South Korea, and Vietnam if you are eligible for Lifeline and/or ACP. ACP recipients get access to up to 8GB of data.

TruConnect serves 37 states, Puerto Rico, and the U.S. Virgin Islands. There are no activation fees, but there is a minimum cost of $10.01 for a tablet from TruConnect.

All TruConnect plans come with two months of free Amazon Prime. Upgrade to a TC+ plan for just $1/month or purchase a tablet, and you'll get Amazon Prime free every month as long as you have an active TruConnect subscription.

Qualify for TruConnect if you are enrolled in:

Medicaid / Medi-Cal

SNAP / CalFresh

Federal Public Housing Assistance or Section 8

Supplemental Security Income (SSI)

Veteran and Survivors Pension Benefit

Multiple Tribal Assistance Programs

And more

TruConnect is BBB-accredited since 2021 and carries an A+ rating.

20. Verizon Wireless

Verizon Wireless offers Lifeline-discounted free government smartphone service in nine states and the District of Columbia. Plans range in price by state. You can bring your own compatible device or choose a free or discounted cell phone online (options vary but are from top brands like Apple, Samsung, and Motorola).

Verizon also offers Lifeline plans for home phone and Fios internet in 11 other states.

Verizon Wireless is not rated by the BBB. However, Verizon Communications has been accredited with the BBB since 1929 and carries an A+ rating.

Don’t qualify for ACP? Where to find discounts for cell phones and low income cell phone plans

Here are additional programs and providers who offer discounted or free phones for low-income households, along with cell service:

Mint Mobile

Mint Mobile offers an introductory 3-month phone plan for as low as $15/month on the T-Mobile 5G network. After the three-month period, customers can choose between 3-, 6-, and 12-month plans starting at $15/month. Plans include unlimited talk and text. Data ranges from 5GB to unlimited based on the plan you select. You’ll pay taxes, fees, and shipping to get set up.

Mint Mobile allows its customers to keep their current phone, phone number, and contacts as long as the device is unlocked and compatible with T-Mobile service. You can also buy a new iOS or Android phone starting at $99.

You can upgrade your Mint Mobile plan at any time if you need more data, and you can switch to a smaller plan when it’s time to renew.

Mint Mobile is not rated by the BBB.

Red Pocket

You can buy a Red Pocket prepaid plan starting at $2.50 per month through eBay and keep your old phone, number, and contacts. These plans include a high-speed SIM card and activation code to connect with one of Red Pocket’s three networks, which include AT&T and Sprint coverage.

Red Pocket also offers monthly plans starting at $20/month for AT&T compatible and most unlocked phones. New phones through Red Pocket start at $349.

Red Pocket is BBB-accredited since 2013 and carries an A+ rating.

FAQs about free smartphones and discount plans for low-income families

Can you get free phones online?

Yes, you can get free phones online. Providers mentioned in this post like AirTalk, StandUp Wireless, and Assurance Wireless allow you to sign up for service online and choose a free phone and free or discounted phone plan. Your phone will be mailed to your address along with instructions for activation.

How can I get a free government phone?

Apply with the Lifeline National Verifier. You will need to show proof of income and any government or Tribal assistance you receive.

Once accepted, you can apply directly with a participating wireless provider of your choice to receive a free phone or a discounted cell phone and/or service.

Can I get a free government iPhone?

While there are thousands of people each month who want to know if they can get a free government iPhone, the answer is likely no, unless your provider offers free iPhones as part of its Lifeline Assistance program, available in 36 states, Puerto Rico, and the U.S. Virgin Islands.

AirTalk Wireless is one of those programs that offers a free government iPhone, but it is an older model.As of January 2024, the current offerings are:

iPhone SE

IPhone SE 2

iPhone 6

iPhone 6s

iPhone 6s Plus

iPhone 7

iPhone 7 Plus

iPhone 8

iPhone offerings are subject to change.

However, qualifying individuals can get a free Android phone or a discounted iPhone through the FCC’s TruConnect program, which includes 14 GB of monthly data. Customers who qualify for Lifeline Assistance also receive unlimited talk, text, and free international calling to select countries.

Can you get a free phone with EBT or food stamps?

While you can’t get a free phone with EBT (Electronic Benefits Transfer), having an EBT card means you have SNAP benefits. People with SNAP benefits qualify for the Lifeline and ACP programs which offer free phones to eligible applicants.

Can I get free phones for my kids?

Yes, you can get free phones for your kids.

Assurance Wireless, T-Mobile, and SafeLink participate with Lifeline and ACP making it easy to get a free phone if you qualify based on income. However, you can only use one Lifeline/ACP benefit per household. If you are using that benefit for yourself, you still have options to get a free phone for your kids:

Bottom line: How can I get a free phone without paying?

There are a few ways to get a new, free phone. If you meet income requirements for Lifeline, many of those plans come with a free smartphone.

If you don’t qualify, you still have options:

Sign up for a new cell phone plan with a different wireless provider and a new phone is often part of the deal, however it may require a new phone number and you won't get the latest model

Use a service like Best Buy Trade-In or Amazon Trade-In to get cash for your old phone and then use that money to buy your new phone

Check with different wireless providers about phone exchange programs where you can turn yours in and get a new phone when you become a customer

Research special shopping events like Black Friday, Cyber Monday, and after Christmas sales for free phone deals

Need more resources? Check out these helpful articles:

Many wireless carriers that provide free phones allow you to sign up for service online. Your phone will be mailed to your address along with instructions for activation.

How can I get a free government phone?

Apply with the Lifeline National Verifier. You will need to show proof of income and any government or Tribal assistance you receive. Once accepted, you can apply directly with a participating wireless provider of your choice to receive a free phone or a discounted cell phone and/or service.

Can I get a free government iPhone?

While there are thousands of people each month who want to know if they can get a free government iPhone, the answer is likely no, unless your provider offers free iPhones as part of its Lifeline Assistance program, available in 36 states, Puerto Rico, and the U.S. Virgin Islands.

What is the best free government phone company?

The best free government phone company is the one that meets your specific needs for communication. That said, SafeLink Wireless is one of the best free wireless and smartphone providers. SafeLink has an A+ rating with the Better Business Bureau, serves a wide coverage areas, and has a useful an app to help manage your account.

What cell phone companies offer free phones?

These wireless providers, among others, offer free phones: American Assistance, Assurance Wireless, SafeLink, and more.

How can I get a new phone for free?

If you struggle to pay for a phone or phone plan, apply for the federal Lifeline Assistance Program using the Lifeline National Verifier.

Wondering how to make money as a teenager? Or get your kid out of the house and learning real life skills?

Whether you have to get a traditional part-time job to help your family pay bills or you’re looking for a flexible side hustle so you can save money for college, there are plenty of good jobs for teens.

We put together a list of the best jobs for teens so you can start earning money now:

Making money as a teenager can be a great way to learn important skills, like budgeting and time management. Having a job also allows you to contribute to your family’s bills if needed and save money for your future.

Learn life lessons

“Doing odd jobs and part-time work can help teenagers build a portfolio of skills that pushes their careers forward,” says Pareen Sehat, a registered clinical counselor at Well Beings Counselling, a private practice based in Canada with multiple locations and telemedicine services.

“These jobs help them learn time management, communication and often teamwork. All of these are crucial professional skills,” Sehat says.

A study by the Employment Policies Institute found that teens who worked a part-time job experienced long-term benefits like:

Higher future hourly wages (20% higher 6-9 years after graduation)

Increased annual earnings

Less time spent out of work

Joanne Frederick, a licensed mental health counselor in Washington, D.C., who works with adults, families, and children, says having a job may help a teen determine what they want to do in the future, another valuable life lesson.

“They have insight and experience, which allows them to scope out what they potentially want to pursue,” she says.

Frederick adds that teens can gain confidence and independence from earning money.

“Getting a job as a teen is a self-esteem booster,” she says. “Teens feel more empowered and have a feeling of accomplishment. It paves the way to becoming more independent.”

Plus, teenagers who work and earn their own money tend to be more financially literate than teens who don’t, Sehat says.

“They’re able to make better decisions and have more control over their expenditures,” she says. “This gives them an edge when they move into their professional lives.”

Learn value of money

A part-time job can also teach you about the value of money. If you work, you can learn about concepts like saving and budgeting.

“Money doesn’t grow on trees, and having a job as a teen allows one to understand that,” Frederick says. “You have to make your own decision on whether you want to purchase an item or save for something else. You are taught to budget and prioritize finances.”

Build character

“When taking on a job, you are understanding responsibility and accountability,” Frederick says. She says a job can help you learn important life skills like:

Overcoming obstacles and managing problems

Become more responsible with time management

Improve social skills

Families and kids are poor and need money

According to U.S. Census data, 16.1% of U.S. children ages 18 and younger were living in poverty in 2020, nearly 2% more than in 2019.

“A teen may come from a family where a parent is deceased and there is only one income, or there may have been a divorce where alimony is not being paid or is very limited,” Frederick explains.

She says even in a dual-income home, both incomes may not be enough to cover all family expenses, especially if there are numerous children.

Frederick adds that if a parent has a serious illness or a child with special needs, then money and resources might be required for their care. And if a parent is dealing with substance abuse disorder or has lost a job, then that might also necessitate additional income from a teen, Frederick says.

If your family is struggling financially, we put together a list of resources to help:

Traditional jobs for teens, like fast food and retail jobs, usually come with set hours — so they’re good options if you have time to dedicate to a job after school or on the weekends. Side hustles, like babysitting and lawn care, are typically more flexible.

All of the salary estimates in this section are from Payscale.com.

Fast food

About 30% of fast food job workers are teens ages 16 to 19, according to Hireteen, a resource for teen jobs. Popular fast food jobs for teens include cashier, cook, and crew member.

National average hourly pay: $9.40

Restaurant server/host/hostess

Another traditional job for teens is working at a restaurant. At a restaurant, you might be asked to serve food, greet customers as a host, bus tables, wash dishes, or check customers out at the cash register.

National average hourly pay: $9.71

Retail sales

Working at a retail store is a good way to earn money as a teen. At a retail job, you may be asked to operate the cash register, fold clothes, stock shelves, or assist customers.

National average hourly pay: $11.83

Grocery store

Grocery stores are another good place to look for a job if you’re a teen. As a grocery store clerk, you may be asked to stock merchandise, take inventory counts, or bag groceries for customers.

National average hourly pay: $11.88

Movie theater

If you love movies, then consider getting a job at your local movie theater. As a movie theater associate, you might be asked to man the cash register, collect tickets, sell concessions, set up displays, or clean up the theater.

National average hourly pay: $11.82

Side hustles for teens

A side hustle is a small job you can do to make extra cash. It usually requires just a few hours of your time a week, unlike a full-time job. You usually get paid quickly, and some of the jobs fluctuate by season. For example, shoveling snow for neighbors is an excellent way to make extra money during the winter.

It’s a good option for teens because it teaches them how to earn money, helps them build a good work ethic, and improves their level of responsibility. Plus, it gives them the opportunity to try a lot of different things and find something they might want to pursue on a more full-time basis.

Here are some of the best side hustles for teens:

Babysitter

Babysitting can be a good side hustle for teens if you like to work with children. You can find clients through friends and relatives, by putting up flyers around your neighborhood, or by creating a profile on Care.com.

If you’re reliable, your clients may recommend you to other families — resulting in more business for you.

National average hourly pay: $8 to $18, depending on age and experience

You can earn cash by offering landscaping services, like lawn-mowing, around your neighborhood. Mowing lawns is an activity that many homeowners don’t like doing because it’s time-consuming and labor-intensive. Most lawns need to be mowed every one to two weeks, so this can be steady work.

National average hourly pay: $10 to $15

Rake leaves

Another landscaping service that can make for a good side hustle is raking leaves in the fall. Similar to mowing lawns, it’s something many homeowners don’t like doing — so they’re usually happy to hire a teen to do the work.

National average hourly pay: $10 to $15

Shovel snow

If you live in a colder area, consider shoveling snow in the winter. People usually dislike having to clean the snow out of their driveways and front sidewalks since it’s labor-intensive — and potentially dangerous for older homeowners — so this can be a steady side hustle for teens in the colder months.

National average hourly pay: $10 to $15

Walk dogs

Walking dogs can be a good side hustle for teens, especially if you like animals. Dogs need to be walked every day, sometimes multiple times a day — and pet-owners often need help with this while they’re at work.

As with babysitting, you can find dog-walking clients by putting up flyers or asking friends and family to recommend you. You can also download an app like Wag! or Rover to find dog-walking and dog-sitting gigs in your area. If you’re reliable, you may be able to grow your business by word of mouth.

National average hourly pay: $10 to $25

Summer jobs for teens

If you don’t have time to work during the school year but would like to make some extra money during the summer, there are plenty of seasonal gigs you can get.

Some government agencies also collaborate with businesses to offer summer work programs. States may use funds from community block grants to create a summer jobs program. Check with your local social service agency to learn more.

Check out these popular summer jobs for teens:

Concession stand worker

One of the most popular summer jobs for teens is working at a concession stand. Places like amusement parks, sports arenas, swimming pools, and concert venues have concession stands that sell foods like hot dogs, popcorn, and cotton candy. As a concession stand worker, you may be asked to take orders, handle payments, or greet and serve guests.

National average hourly pay: $11.28

Lifeguard

Working as a lifeguard at your local pool can be a great summer job for teens. Just keep in mind that becoming a lifeguard requires special training. You’ll need to get certified, which you can do through an organization like the YMCA or Red Cross. Training involves passing a pre-swimming skills test and getting certified to do CPR. Certification costs are usually in the $100 to $200 range.

Because working as a lifeguard requires certification and comes with a lot of responsibility, you can usually earn more than minimum wage at this seasonal job.

National average hourly pay: $14.28

Camp counselor

Working as a camp counselor during the summer can be a fun way to earn money as a teen. As a camp counselor, you may be asked to supervise a group of kids and participate in activities, like swimming, sports, and arts and crafts, with them.

National average hourly pay: $10.23

Golf caddy

Golf courses often hire teens as golf caddies during the summer months. As a golf caddy, you may be asked to carry a golfer’s bag and clubs around the golf course, keep their clubs clean, and locate their golf balls. This is one of the better-paying summer jobs for teens.

National average hourly pay: $19 (Ziprecruiter)

Amusement park employee