If you’re a freelancer or entrepreneur, or thinking about becoming one, it’s vital to protect yourself and your business.

Here are the top disability insurance providers for self-employed workers:

- Northwestern Mutual

- Guardian

- Mutual of Omaha

- Assurity

- Breeze

Which is the best?

Quick answer: You need disability insurance as well as life insurance. Those who do not have disability insurance through a job, including the self-employed, can find individual coverage through reputable companies for an affordable price. Breeze disability insurance plans start at $9/month for people aged 18 to 60 years old, with monthly benefits ranging from $500 to $20,000.

In the market for life insurance? Bestow's rate is as low as $10/month and policies up to $1.5 million, with guaranteed no medical or lab exam. Read our Bestow review.

Here’s what you need to know about disability insurance for the self-employed and Breeze insurance:

What disability insurance Breeze offers

- Breeze long-term disability terms

- Breeze long-term disability optional riders

- Breeze Critical Illness Insurance

How much a Breeze disability insurance policy cost

Pros and cons of Breeze insurance

Disability insurance for self-employed individuals

- How much disability insurance do I need as a self-employed individual?

- How much does disability insurance cost for individuals who are self-employed?

- How do I get disability insurance?

Common questions about disability insurance

Bottom line: Is disability insurance worth it?

What is Breeze?

Breeze is an insurtech start-up that specializes in long-term disability insurance. Founded in 2019, it is underwritten by Assurity Life Insurance Company, which has been in business for more than 125 years and has an “excellent” rating from A.M. Best.

Currently, Breeze is the only insurance company offering a 100% online application process. Thanks to fully automated underwriting, Breeze can provide instant quotes and set you up with a long-term disability insurance policy in as little as 15 minutes from start to finish. You probably won’t even need to take time out from your workday for a doctor’s exam or blood work.

Bonus: If your income is under $4,000 per month, you don’t have to provide any proof of earnings. Those making more than $4,000 monthly have to provide just a pay stub or tax return.

Here are a few of the free features in every Breeze policy:

- Presumptive disability: In the case of loss of eyesight, hearing, speech or limbs, there’s no elimination period – benefits begin immediately.

- Partial disability: If you return to work part-time after full disability, you’ll get a monthly benefit for up to six more months.

- Home modification: This is a benefit for those who have to retrofit your home to accommodate a disability.

- Survivor benefit: If you die after receiving payments for at least 12 months, Breeze pays a lump sum equal to six times the monthly benefit.

Based on the information you provide, Breeze will give you personalized options (good, better, best) that you can customize. For example, you can add options like a non-cancelable policy or “guaranteed insurability,” which lets you buy more coverage to add to your base policy monthly benefit.

What disability insurance Breeze offers

Breeze long-term disability terms

Breeze primarily offers long-term disability insurance coverage. While 10-year terms are the most common, Breeze does offer a variety of other terms as well:

- 1-year term

- 2-year term

- 5-year term

- 10-year term

- To age 65

- To Age 67

For most individuals, a 10-year term will offer an appropriate level of coverage, but other term lengths have their own role to play.

For example, if you have just 1, 2, or 5 years until you will be eligible for retirement benefits, then those shorter terms can help you protect your ability to bring in money during those final years. Likewise, if you are particularly risk-averse, longer terms that cover you until you are full retirement age (65 or 67 years old, depending on when you were born), then those policies can also be a good fit.

Breeze long-term disability optional riders

Breeze also offers a number of optional riders that you can add to your policy in order to account for a variety of possible scenarios. While the addition of riders will increase your total cost, they can often be a good idea. The optional riders offered by Breeze include:

- Automatic Benefit Increase Rider: Each year you maintain your coverage, your base monthly benefit will increase by 5% (of the original amount) until the monthly benefit has increased to double the original amount.

- Guaranteed Insurability Rider: This rider gives you the option to increase your monthly benefit by purchasing additional coverage at a later date if your salary increases, essentially locking in your ability to purchase disability insurance. These increases won’t require evidence of insurability.

- Own Occupation Rider: Own occupation insurance provides disability insurance in the event that you become disabled and can no longer work in the occupation you held before becoming disabled—even if you can technically work in a different occupation. The addition of this rider extends the own occupation period of your policy from two years through the full term.

- Residual Disability Benefit Rider: This rider provides a residual disability monthly payment in the event you become residually disabled and the elimination period has been satisfied.

- Supplemental DI Rider: This rider provides additional insurance on top of the monthly benefit provided by social insurance benefits in the event you are totally disabled.

Breeze Critical Illness Insurance

In addition to long-term disability insurance, Breeze also provides critical illness insurance. This is insurance that is specifically designed to pay you a cash benefit if you become afflicted by a serious illness that impacts your ability to work.

Conditions covered by Breeze’s critical illness insurance policies include:

- Heart attack

- Major Organ Transplant

- Angioplasty

- Stroke

- Paralysis

- Coma

- Kidney failure

- Coronary artery bypass surgery

- Advanced Alzheimer’s disease

- Cancer (invasive and non-invasive)

If the event that you are afflicted by a covered condition, you will receive a lump-sum cash payment that you can either use to cover you medical expenses, regular monthly expenses, or other things.

How much a Breeze disability insurance policy cost

Plans start as low as $9 per month for people aged 18-60 years old. Monthly benefits range from a low of $500 to a high of $20,000.

Ultimately, the cost of your monthly premium will depend on a number of factors, including:

- Your age and health at the time of application

- Your occupation

- The coverage amount (monthly benefit) you choose

- The benefit period or term you select

- The elimination period/waiting period you choose

- Whether or not you add any additional optional riders

How Breeze works

Getting an initial quote through Breeze is 100% online and takes less than 5 minutes from start to finish.

To get your initial quote, provide:

- Birthdate

- Gender

- Work status (whether you are an employee, a business owner, or an independent contractor)

- Type of work (professional, technical, light labor, labor)

- How many hours you work per week

- Net annual income (income minus taxes, work-related expenses, pre-tax retirement contributions, etc.)

- Zip code

- Whether or not you use nicotine

- Whether you are looking to protect your future, purchase coverage during maternity leave, or are looking for financial assistance because you are currently disabled

You’ll then receive three different recommended coverage options, designed to fit within your budget. You can customize these options easily by adjusting the term length, coverage amounts, elimination/waiting period, and adding optional riders.

If you’d like to proceed, just click “Apply Now” to begin the full application. You’ll be asked questions about whether or not you have ever:

- Filed for bankruptcy

- Had a heart attack or stroke (in last 5 years)

- Been diagnosed with cancer (in last 5 years)

- Used cocaine, heroin, or other illegal drugs (in last 5 years)

- Been charged or convicted of a felony (in past 10 years)

- Are currently on probation

- Been diagnosed or treated with diabetes (in past year)

- Ever been diagnosed with AIDs/HIV-related conditions

You will then create an account by providing your name, email address, phone number, and physical address. At this point, you’ll need to confirm your previous answers, and provide some additional details about your:

- Employment status

- Legal documents (driver’s license, Social Security Number)

- Lifestyle

- General health & health history

You will also need to consent to Breeze obtaining relevant information from third parties (such as health information, driving records, credit history, etc.).

Upon completion of these questions, if you qualify for coverage Breeze will provide you with a final quote.

Pros and cons of Breeze insurance

Pros of Breeze

- Breeze’s application process is entirely online

- Breeze rarely requires medical examinations

- It takes less than 5 minutes to complete the initial application and get a variety of quotes

- Policies are extremely affordable, starting at just $9 per month

- A variety of term lengths (1-, 2-, 5-, 10-year, etc.) allow you to choose the right policy for your needs

- Additional riders (automatic benefit increase, guaranteed insurability, own occupation, residual disability benefit, supplemental DI) give you even more customization options

- Breeze offers critical illness insurance coverage in addition to long-term disability insurance, providing even more coverage options

Cons of Breeze

- Breeze does not offer short-term disability coverage

- If you are denied coverage during the application process, you will not immediately receive an explanation why. That being said, you will receive a letter in a number of weeks with more details about Breeze’s decision.

Breeze insurance reviews

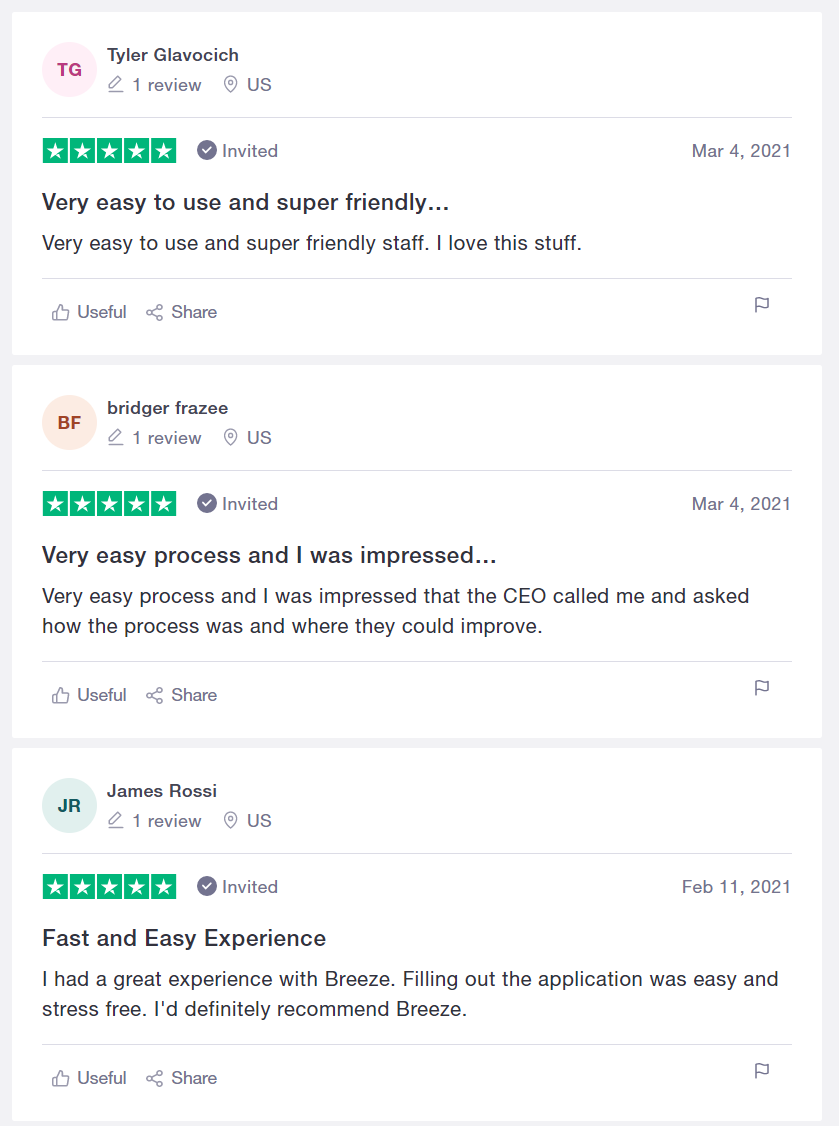

Breeze unfortunately does not currently have a profile with the BBB. That being said, Breeze does have a profile on Trustpilot, where it maintains an average rating of 4.5 out of 5 stars based on more than 45 reviews.

Most reviews of Breeze on Trustpilot are very positive. Below are a number of example positive reviews:

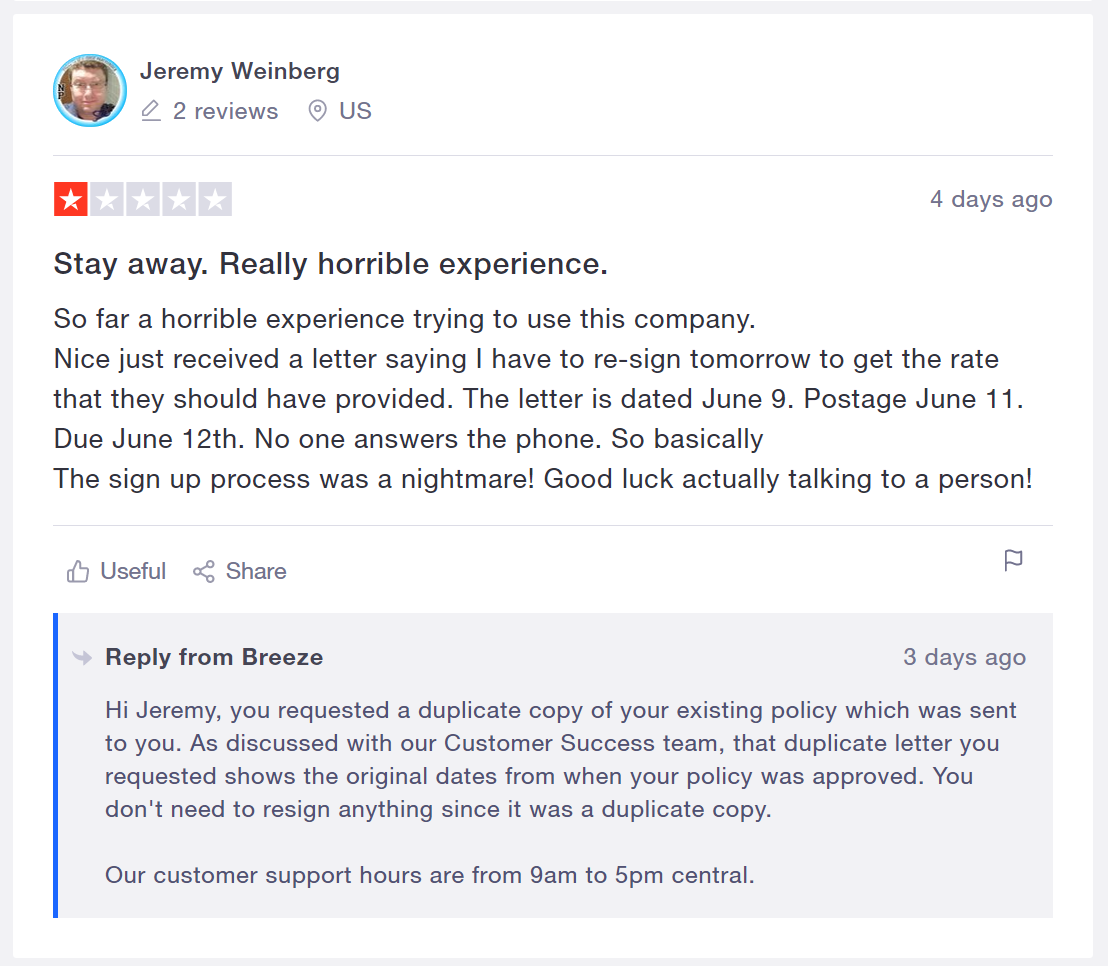

For comparison, below is a screenshot of the single negative review which was left (along with Breeze’s response):

Disability insurance for self-employed individuals

Short-term disability insurance, which is generally available through an employer, provides benefits for up to one year after a short “elimination” (waiting) period.

Long-term disability insurance may also be offered through an employer, but can easily be purchased by individuals. It has a longer elimination period (generally 30 to 90 days), but continues to pay out until the disability ends or the insured reaches retirement age.

The benefits will depend on the kind of insurance you buy. For example, some policies will pay if you can’t work in your current occupation, while others will pay only if you can’t work in any job you’re qualified to do. It’s essential to compare apples to apples when researching the cost of disability insurance.

Still have a day job but looking at self-employment? Consider buying long-term disability insurance now, so you can take it with you when you segue into solopreneur-ing. Specify a non-cancelable, guaranteed-renewable policy. That way, your coverage will continue as long as you make your payments.

If you’re already self-employed, look at getting disability insurance right away. As noted, you’ll likely get the lowest premiums when you’re young. For example, Breeze offers policies beginning at just $9 per month, and you can apply online in minutes.

Career-level jobs that are great for moms

How does disability insurance work for individuals who are self-employed?

If illness or injury strikes, you can file a claim for disability benefits with supporting documents from your doctor. After the “elimination” (waiting) period ends, your monthly payments begin.

Benefits are paid for the number of years specified in the policy; in some cases, that could mean until you reach full retirement age. Some policies also pay for related expenses, such as home modification (e.g., a wheelchair ramp) or vocational rehabilitation.

When you’re cleared to go back to work, you notify the insurance company to end the payments. Some policies provide partial benefits if you go back to work part-time, or if you can work only in a different kind of job.

How much disability insurance do I need as a self-employed individual?

As noted, a typical policy covers as much as 60% of your current income, up to a cap set by the company. Before choosing your benefit level it’s important to add up all essential expenses. (If you’ve already got a budget plan in place, you’ll know exactly how much it costs to support your lifestyle.)

The earlier you buy the policy, the less it will cost. That’s because the older we get, the more likely we are to become sick or injured. For example, suppose in your late 20s you’re treated for a repetitive strain injury. When you apply for disability insurance at 35, RSI might be excluded from coverage.

Note: When you buy your own disability insurance policy, any benefits paid out are not taxed. However, benefits from an employer-paid policy are subject to income tax.

How much does disability insurance cost for individuals who are self-employed?

Generally speaking, a policy will run between 1% to 3% of your salary.

If you are self employed, disability coverage is based on your income as reported on the past two years of your tax returns. For example, for a sole proprietor, use your 1040 and Schedule C. For an S Corp, your 1040, W2 and Schedule E are used.

If you have been self-employed for less than two years, the disability insurer will ask for recent W2s or other documents.

Unlike many health insurance premiums, disability insurance premiums are not tax-deductible. However, any benefits paid through an individual disability insurance plan are tax-free.

How do I get disability insurance?

Disability insurance for the self-employed is available through traditional insurance companies, independent brokers, unions and “insurtech” companies like Breeze.

Look for a company with a superior financial rating. Agencies like Moody’s and A.M. Best rate insurance companies; just like in school, a grade with an “A” in it indicates the better-performing companies.

In most cases you’ll need to show two years’ worth of tax paperwork to prove you earn a living as a self-employed person. You’ll also need to provide a family medical history and both personal and professional information.

Some level of medical examination, including blood tests, is generally necessary. (But not always; Breeze rarely requires an exam.) You’ll probably need to authorize the release of medical records and, in some cases, your driving record and credit report. Breeze only uses social security numbers to verify identity — not qualify you for coverage.

Google the phrase “disability insurance for the self-employed” and you’ll find traditional insurance companies offering to match you with agents in your city. At that point you’d go through the process noted above.

11 steps to survive financially for single moms

Common questions about disability insurance

What is disability insurance?

Disability insurance is just what it sounds like: a policy meant to replace a portion of your income if illness or injury leaves you unable to work. Each insurance company has its own limits, but typically disability insurance covers up to 60% of your pre-tax salary.

Disability insurance is part of your overall financial health. Also make sure you are:

- Paying off debt.

- Have a $1,000+ emergency fund, and a basic investing strategy.

- Get life insurance.

- Have home or renters insurance.

Disability insurance is a common workplace benefit, often partially or completely paid for by the employer. But disability insurance for the self-employed is a different matter, because there’s no employer to arrange it.

No one likes to think about becoming disabled. Yet according to the Social Security Administration, a little more than 25% of today’s 20-year-old workers will become disabled before retirement.

Workers’ Compensation only covers injuries and illnesses that are directly caused by the workplace. Social Security Disability Insurance is another benefit source, but only about 1 in 3 applicants qualify, the average processing time is more than 18 months, and the average SSDI benefit is $1,197 per month.

What does disability insurance cover?

The insurance covers illness, injury and other conditions (such as pregnancy) that keep you out of the workforce. According to data collected by the nonprofit Council for Disability Awareness, the top five reasons for long-term disability claims are:

- Musculoskeletal disorders (29%)

- Cancer (15%)

- Pregnancy (9.4%)

- Mental health issues, such as depression and anxiety (9.1%)

- Injuries such as sprains, fractures, and strains of muscles and ligaments (9%)

What is not covered by disability insurance?

Typically, any injury or illness originating in these situations is not covered by disability insurance:

- Fighting in a war.

- While committing a crime, participating in a riot, or while in jail.

- Self-inflicted or intentional injury to yourself.

Is disability insurance based on income?

Yes, you will need to prove your most recent income to qualify for any sum of disability insurance.

The monthly benefit payout amount should be about 60% of your take-home pay. You may be able to purchase more disability insurance to cover increases in the cost of living.

Bottom line: Is disability insurance worth it? Is Breeze a good insurance company?

Disability insurance for the self-employed is not just worth it – it’s crucial. When self-employed workers can’t bring in money, they can’t get paid. The business you worked so hard to build could be heavily affected – or maybe even collapse – if you are unable to work. Having disability insurance could mean the difference between financial survival and financial disaster.

If you’re in the market for disability insurance for the self-employed, Breeze is the fastest and easiest way to do it. Within a quarter of an hour you can obtain coverage that provides peace of mind and lets you get back to the business of growing your business.

Breeze is an insurtech start-up that specializes in long-term disability insurance. Founded in 2019, it is underwritten by Assurity Life Insurance Company, which has been in business for more than 125 years and has an “excellent” rating from A.M. Best.

If illness or injury strikes, you can file a claim for disability benefits with supporting documents from your doctor. After the “elimination” (waiting) period ends, your monthly payments begin. Benefits are paid for the number of years specified in the policy.

As noted, a typical policy covers as much as 60% of your current income, up to a cap set by the company. Before choosing your benefit level it’s important to add up all essential expenses.