Heirloom, inherited, estate and antique jewelry, as well as jewelry you received as a gift but never wear, broken chains and divorce-tainted wedding bands are often best sold instead of collecting dust — especially since gold prices reached record highs nearing $4,400 this year.

In this guide, we present an overview of how to sell your gold, diamond, pearl and gemstone rings, necklaces, chains and earrings, and unpack at the best places to sell jewelry.

Quick take: Our top choices for selling jewelry

- Best for immediate cash: A pawnshop or gold buyer in your community can offer helpful service and a very fairprice.

- Best online jewelry buyer: CashforGoldUSA. It’s family-owned, based in the United States and pays fast. In a related post, we explain how CashForGoldUSA works and what the selling experience was like for our writer.

Tips for selling your selling your jewelry

Here is how to assess the value of your gold, diamond, gemstone or other jewelry:

1. Understand what your jewelry is worth

It's important to understand exactly what your jewelry is made of, and the approximate market value of the karat of gold and/or diamonds, weight, and in some instances, the brand.

If your item is worth about $1,000 or more, it can be worthwhile to invest in a jewelry appraisal or, for diamonds, a lab report — documents that spell out the value of your item.

Selling gold jewelry

Most gold jewelry, unless it very significant in size, a special design or made by a noteworthy brand like Tiffany or Cartier, is likely to be bought for its scrap gold value. This includes gold chains and necklaces, gold wedding bands and most gold charms and brooches.

This is good news if your item is dated, broken or small — it is still always valuable and will get you cash.

Familiarize yourself with gold hallmarks, or stamps, that signify the karat — even if you think you know what you have.

Selling diamond jewelry

Familiarize yourself with the market value of diamonds (which have dramatically fallen in recent years), as well as understand the cut, carat, clarity and other qualities of your stone.

If your chain features diamonds of at least .5 carat center stone, a diamond appraisal will evaluate the stones on the 4 C’s: color, cut, clarity, and carat and can be helpful in the sales process — though they cost around $200 or more.

We published a guide to selling diamonds: More on how to sell diamonds and diamond jewelry.

You can always take your jewelry to a pawnshop or jewelry store where they can weigh your necklace and give you an estimate — or a quote to buy.

As for pearl or gemstone jewelry, unless your ring, earrings or necklace are very special with a very large and valuable center stone, or by a famous designer, the stone is likely worthless, though the precious metal will be worth the spot value.

2. Work with a reputable buyer

Sources of information on buyers include:

- Better Business Bureau

- Trustpilot

- Yelp!

- Google searches

- Friends

- Family

The next section explains where to find gold buyers.

3. Don’t accept the first offer + negotiate

When it comes to selling your necklaces for cash, you can always negotiate any offer, including with online buyers. Here are some tips for how to negotiate prices:

- Express appreciation: Start by thanking the buyer for their offer. Being polite and respectful can create a more positive relationship for negotiation.

- Ask for clarification: Politely ask the buyer to explain how they arrived at their offer. This can help you understand their perspective and give you an opportunity to point out any unique or valuable aspects of your necklace.

- Mention any special features or history: Your sentimental attachment to the piece won't add value, but if your necklace has unique features, such as a rare design, special craftsmanship, or historical significance, be sure to mention them.

- Research current market prices: Knowledge of the current market price for gold can be a powerful negotiating tool. You can say, “I've done some research, and I know that the current market price for gold is [mention the price]. Can you match or come close to that?”

- Mention competitive offers: If you've received other offers or have the option to sell to multiple buyers, bring in documentation. Saying something like, “I have another offer from a different buyer for [mention the offer amount], but I'd prefer to sell to you if we can work out a better deal” may encourage them to offer more.

- Be willing to walk away: Express your willingness to walk away from the deal can put pressure on the buyer to make a better offer. Try: “I appreciate your offer, but I was hoping for something closer to [your desired amount].” The pack up to leave.

- Negotiate incrementally: Instead of outright rejecting the offer, you can propose a counteroffer that's slightly higher than their initial offer but still reasonable. Show a willingness to compromise.

6 places to sell your jewelry safely

There are pros and cons of selling to different types of business. Rest assured there are many quality buyers both locally and online.

Our recommendations are based on:

- Online reviews from customers

- Speed to cash

- Better Business Bureau ratings

- Reports from reputable publications

- Age of the company

- Location of the jewelry buyer (based in the U.S.)

- Ease of use of their websites

- Transparency into their process

- Overall sentiment that these are quality businesses that care about their customers

1. Sell to pawnshops

Most pawn shops do buy jewelry, including scrap gold like broken necklaces and inherited jewelry. If you need cash immediately — or are interested in a pawn loan — a reputable pawn broker can be a good option.

- Pro: Quick money, possibility to get your necklace back within 30 days, could get a fair price working with a trusted local business.

- Con: Might get a low-ball offer, you may feel embarrassed dealing with a pawnbroker or being seen in public selling your valuables

2. Sell your jewelry online

There are numerous quality online buyers that will pay you money for your gold, silver, and platinum jewelry. You can consult the Better Business Bureau, Yelp, Reddit and Trustpilot to read customer reviews.

Pros of selling online: Convenience, as with some buyers, you can complete the entire process from home. Some have best-price guarantee, and any quality online jewelry or metals buyer will send a free round-trip mailer and jewelry insurance.

Cons: Takes a few days or more (depending on the buyer)

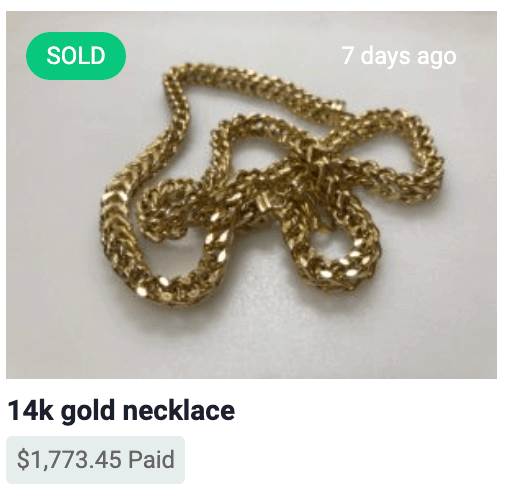

Based on our exhaustive review, CashforGoldUSA.com is our top choice to sell your gold chain online and the best place to sell your gold necklace period. Read our review of CashforGoldUSA.

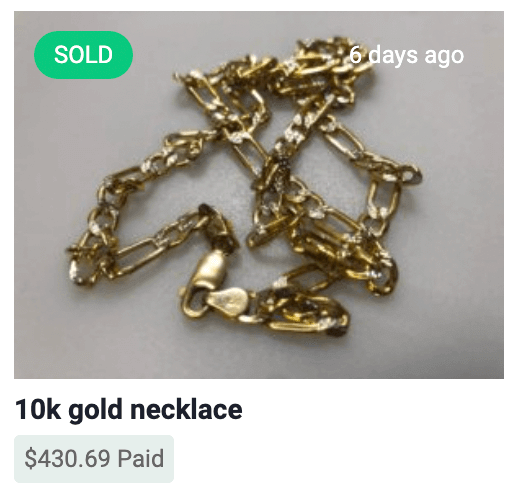

A couple recent sales to CashforGoldUSA:

14k gold chain necklace sold for $1,773.45:

10k gold chain necklace sold for $430.69:

3. Sell your jewelry to your local jeweler

We understand that some people have an urgency, and the best jewelry buyer might be the one that offers the fastest turnaround. In that case, a local jeweler you find “near me” may give you a fair value of your jewelry in cash on the spot.

Selling your gold chain, diamond ring or other jewelry at a local jewelry store is a good option, especially if you know a business you trust.

- Pro: Could be a fair payout, quickly. Some jewelers offer trade-in deals.

- Con: Might not get highest offer, and it can be embarrassing to have to sell your jewelry before people you know.

4. Sell to cash-for-gold stores

Cash for gold stores can give you quick cash but have a reputation for low payouts. You can always get a quote, negotiate and shop around.

- Pro: Immediate cash, local

- Con: Payout may be low

5. Local or online auctions

If your gold necklace or chain is pretty standard, nothing special, a gold buyer will most likely offer a payout based on the day's spot gold price, and send it to a refinery to melt down.

However, if you have a significant piece of jewelry or a loose diamond that will sell for at least $1,000, or is a special antique, a marked brand or is a popular style, it is possible a local or online jewelry auction platform may be interested — especially if your necklace is part of a larger estate collection.

- Pro: Possibly could fetch a higher price

- Con: Not immediate cash, may not sell for as much as you like

6. Sell directly

You can always post your chain and try to sell it directly to individuals, or through antique or consignment stores. Check out sites like:

- Facebook Marketplace

- ebay

- Craigslist

- Poshmark

- Mercari

Pros and cons, of course:

- Pro: You may get a higher price, and you can do business locally if you prefer

- Con: A lot of work dealing with flaky people, possibly having to package and shipping your item, or it not selling it all.

21 apps for selling stuff online or locally

7 online jewelry buyers

Unless you need the cash immediately, an online jewelry buyer can be the best position to offer you the highest price, as they benefit from not needing expensive retail rent, and you benefit from the competitive online market.

Other benefits of selling to an online buyer include that a quality buyer will provide free, door-to-door shipping, the privacy of never leaving your house, and full insurance. Many rural communities do not have many local options.

Here are some of the most reputable online buyers:

1. CashforGoldUSA

We like this family-owned company for many reasons, including that they give a 10% bonus when you send in your shipment within a week and have helpful customer service and have many options for shipping and payment.

Pricing and payment

- Get paid within 24 hours

- 10% bonus if you send your item within 7 days

- 100% highest price guarantee

Reputation

- Better Business Bureau rating of A+

- Founded 2005

- 4.4/5 Trustpilot stars

Safety and insurance

- Free, secure mailer or FedEx package sent to your home

- Buys gold, silver, platinum jewelry, watches, coins and scrap

- Insurance up to $150,000

Value add

- Guaranteed highest price

- If you do not accept their offer, you can get your item back immediately, free of charge

- Your choice of shipping: USPS or FedEx, or print label at home for fastest process

- Accepts all diamonds, gold, sterling silver and gemstones regardless of size or quality (other jewelry buyers have minimum diamond size or resale value)

Read our CashforGoldUSA review.

2. Abe Mor

Founded in 1964, New York-based and family-run Abe Mor has one of the largest presences in the online diamond buyer market.

They accept only diamond jewelry and loose diamonds of at least .50 carats, including designer diamond jewelry — like engagement rings from Tiffany & Co, Cartier, and Harry Winston — but they will pay you for the gold and platinum content of your jewelry if it's set with eligible diamonds.

Abe Mor pros

- A+ BBB rating, zero customer complaints

- Free shipping

- Free insurance up to $50,000 with additional available for purchase

Abe Mor cons

- Does not buy other types of jewelry or gemstones

- Only accepts diamond jewelry at least 0.5 carats in size

- Appraisals are conducted by in-house Abe Mor staff, though you can request GIA authentication

- May reject diamonds if it does not need them in its inventory

- Typical time from shipment to payment is longer than other sites, though Abe Mor will overnight a check upon request

- Pays within 2 to 4 days upon acceptance of an offer

Check out our Abe Mor review.

3. Circa

Circa accepts high-end branded jewelry, as well as diamonds of at least .4 carats, and engagement rings. They will also purchase historical or estate jewelry including pieces such as: Antique, Edwardian, Georgian, Art Nouveau, Belle Epoque, Art Deco, Retro and Modern.

Whether in-person at one of their 23 locations internationally or online, if you accept Circa’s offer, you will be paid immediately via check, bank transfer, or gift card (worth up to 120% of the purchase offer) toward a jewelry purchase from Circa.

If you provide a grading report from the GIA, EGL, IGI, AGS, GSI, GCAL, IIDGR, or HRD, Circa provides a guaranteed offer range.

Circa pros

- A+ Better Business Bureau rating

- Works in partnership with diamond retailer Blue Nile

- Promises to offer a high price to you by cutting out the middleman

- Website's videos and posts create transparency

- Fully insured FedEx delivery — both from you to Circa, as well as returns, when relevant

- 14 physical locations (11 in the U.S. and 3 international)

- Claims that more than 90% of its customers receive a final offer price higher than the midpoint of the guaranteed range (which includes shipping and insurance)

Circa cons

- This buyer only deals in jewelry with a diamond of at least .4 carats

- If you do not have a lab report, you must send in your item for evaluation and grading before an offer is made

- That offer is good for just 7 days, after which you have to start the whole process over again

In short, Circa is a solid company that brings the Blue Nile experience full circle, promising to offer jewelry sellers high prices by removing the middleman.

4. myGemma, formerly WP Diamonds

myGemma, formerly WP Diamonds, has a solid reputation as an online luxury jewelry buyer, and promises to get you a fair price for your diamond or designer jewelry, loose stones (diamonds of at least .5 carats), handbags, watches, and luxury accessories.

However, theirs is a more traditional buyback platform, in that myGemma's in-house team of GIA-trained gemologists and industry veterans will evaluate your jewelry, then make an offer. Take it or leave it.

myGemma pros

- Reputable buyer with an A+ BBB rating

- Clean, easy-to-use site

- Pays cash for your jewelry

- Easy process, including FedEx round-trip shipping, and insurance for the full value of your items

- Choose to do business via email or phone

- Sell in as little as 24 hours: myGemma buys your jewelry directly, which means there are no online listings or auctions to wait for, no haggling or negotiating — simply their best price upfront

- No fees are deducted from your final offer — the amount you hear is the amount you get paid.

myGemma cons

- Evaluation is done by an internal appraiser, not a neutral third-party laboratory like GIA, which Worthy uses

- There is just one offer, not a price set by a dynamic marketplace

In summary, myGemma is a reputable online diamond and jewelry buyer, that has been around for a long time. It is the fastest way to sell diamonds safely online to the experts.

Read our myGemma review to learn more.

6. The RealReal

The RealReal is an online marketplace for luxury resale items, including fine jewelry. The site prices your consigned jewelry based on current market trends, and you get paid a commission up to 70% depending on the list price of your items.

Pros of The RealReal

- Accredited by the Better Business Bureau with an A+ rating

- 4/5 stars on Trustpilot

Cons of The RealReal

- Numerous customer complaints on the BBB site about long wait times to process consigned items, items not being returned in the same condition they were sent, unapproved markdowns, and difficulty resolving issues with customer service

- No guarantee your item will sell — most successful jewelry sales are by professional jewelers or others who have the ability to professionally photograph, display and market their jewelry

- Must schedule an appointment to meet with a representative and be accepted to sell

7. Worthy

If you have jewelry valued at $1,000 or more, including a diamond engagement ring, other diamond or gemstone jewelry, or branded items from Tiffany, Cartier or another high-end jeweler, then consider Worthy.com, an online marketplace where hundreds of vetted buyers bid on your item.

Typically, the center diamond of an engagement ring of at least .5 carats will sell for $1,000. Worthy also accepts lab-grown diamonds of at least 3 carats. Worthy is A+ BBB rated, and insures your item up to $100,000 with Lloyds of London.

Worthy pros

- A+ BBB rating

- 4.6 rating with Trustpilot

- High consumer reviews

- Free lab GIA report

- Cool website that helps you understand the value of your jewelry

Worthy cons

- Takes longer than other platforms

- Some users find the process overly complicated

- Focused exclusively on diamond and high-end branded jewelry

- Strict minimum of items that will sell for at least $1,000

Read our Worthy review.

FAQs about selling jewelry

What is the best way to sell expensive jewelry?

In the past, we have recommended selling expensive jewelry, especially those with large diamonds, or branded, luxury jewelry such as those from Tiffany, Cartier or Buglari through a reputable online jewelry platform like Worthy or myGemma — national companies that can efficiently evaluate your diamond or other jewelry, safely ship it, evaluate it by trusted experts and appraisers.

Before you get too excited, however, note that diamond prices have dropped about 40% since their peak in summer 2022, and buyback prices reflect this change:2

For that reason, we recommend online buyer Diamonds USA, which buys all sizes and qualities of diamonds, quickly, and has a strong reputation, or Worthy.com, which specializes in larger diamonds and name-brand pieces.

Complete guide to symbols stamped on jewelry

Can you sell jewelry to a jewelry store?

Working with a local jeweler can be a solid choice if you have a jeweler you know and trust. This can also ensure a quick, cash sale, and many jewelers offer you a bonus if you chose to take store credit.

However, it may be worth the time to also get a quote from a local pawnshop or send in your jewelry to an online jewelry buyer get a second or third offer.

Is it better to sell jewelry to a pawn shop or jewelry store?

Pawnbrokers have a bad reputation for ripping off sellers — but jewelry stores can short-change jewelry sellers, too. The only way to know which is better is shop around, ask local friends and neighbors for recommendations and compare. Getting a quote does not commit you to selling at any of these options.

Is it safe selling jewelry online?

Selling jewelry online with a reputable buyer that insures your item, gives you a FedEx or USPS tracking number and has a robust online presence including Better Business Bureau and other online review sites. Since the online jewelry buyers rely on these reputation sites, they live and breathe customer service and reviews. I feel confident that the buyers listed on this site are honest and safe.

How much is my gold chain worth? What about a broken chain, or a gold ring?

Basic gold items are generally worth the spot price of gold, minus the buyer's commission — which should be around 20% at most reputable places.

For example, a simple gold chain — broken or in-tact — could fetch you $100 to $200. A men's gold wedding band may get you $100 to $200 as well.

Is it worth selling jewelry online?

Selling jewelry online with a reputable buyer that insures your item, gives you a FedEx or USPS tracking number and has a robust online presence including Better Business Bureau and other review sites.

Sell jewelry online can net a higher payout, convenience of not having to leave your home, and total privacy, since your friends and neighbors won’t see you selling your items in town.

Platinum vs white gold: Which is more valuable?

White gold vs yellow gold: What’s the difference, which is worth more?

Sterling vs plated vs white gold: How to tell the difference

What is the best website to sell used jewelry?

CashforGoldUSA buys all gold, silver, diamond and gemstone jewelry, coins, flatware and tableware via overnight shipping. The Boston-based company has an A+ Better Business Bureau rating and hundreds of high Trustpilot reviews, and promises to pay within 24 hours of accepting terms.

Bottom line: It’s OK to sell your jewelry

Many relationships involve precious jewelry — investments that represented care, love, tradition. These may be romantic or family relationships. Your jewelry may be a gift or an inheritance.

Those engagement rings, watches, necklaces, earrings, gold chains, and bracelets can linger in velvet-lined jewelry boxes for years — or even the remainder of the new owner’s life!

Even if that jewelry is worth tens of thousands of dollars, it is still clutter to you.

It all holds energy, good or bad.

Cleanse out the bad energy, welcome the good.

Even if you are unsure whether the value of the gold or diamonds may go up soon, money in your pocket today is 100% guaranteed, vs the unknown of future prices. Plus, you can pay off debt which saves money in interest, or put money into a 401k or 529, which saves money on taxes — guaranteed.