Compare five trusted casket companies in 2026 to find reliable options, fair pricing, and the right choice for your loved one’s farewell.

Discover how Ascent Funding works and whether it may help students and families cover college education costs.

Diamond prices are plummeting, but you can still get cash for your engagement ring. What to know to feel confident when you sell.

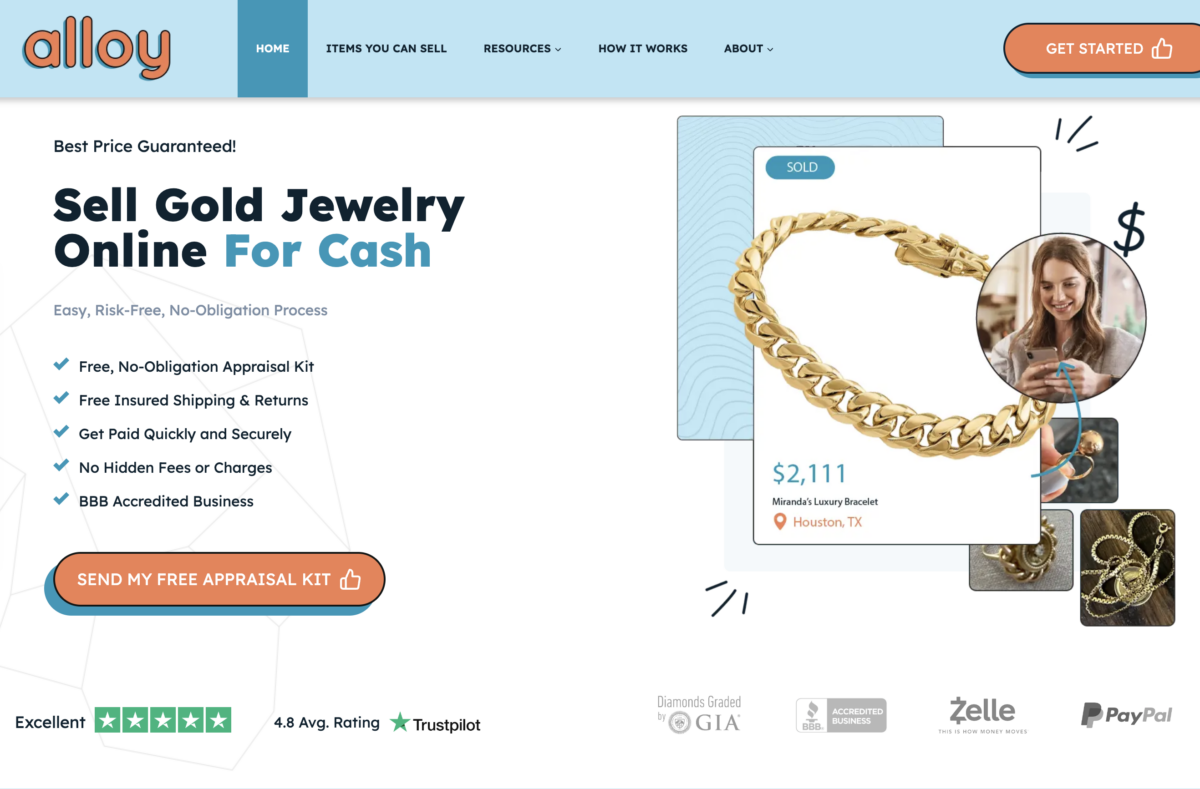

Alloy is a solid option in the online metals buyback space.

FlexJobs is a legit job search site for legit work-from-home jobs, flexible jobs, remote work, and part-time jobs. Here our FlexJobs review.

Compare five trusted casket companies in 2026 to find reliable options, fair pricing, and the right choice for your loved one’s farewell.

Discover how Ascent Funding works and whether it may help students and families cover college education costs.

Diamond prices are plummeting, but you can still get cash for your engagement ring. What to know to feel confident when you sell.

Alloy is a solid option in the online metals buyback space.

FlexJobs is a legit job search site for legit work-from-home jobs, flexible jobs, remote work, and part-time jobs. Here our FlexJobs review.

Thinking about starting a flexible, high-paying, work-at-home career in proofreading? Check out our Proofread Anywhere review.